Introduction

Michelin Statistics: Michelin is one of the world’s largest tyre producers and operates in three sectors: mobility solutions, sustainable materials, and digital fleet services. Michelin was founded in 1889 and maintains its headquarters in Clermont-Ferrand, France, while conducting business operations worldwide across the automotive, aerospace, mining, and industrial sectors.

Michelin experienced significant volatility in 2025 and is currently navigating a recovery phase in 2026 due to economic pressures, declining product demand, and ongoing business changes, including a focus on premium tyre products and expansion into non-tire markets.

Editor’s Choice

- Michelin reported total sales of €25,992 million in 2025, down 4.4% year over year.

- Sales volume contraction resulted in a financial loss of €1,289 million, a 4.7% decrease.

- The positive price-mix effect added €827 million, reducing the impact of volume decline.

- The company experienced a revenue decline of €817 million, representing a 3.0% loss due to currency fluctuations.

- The company’s operating income for this segment decreased by 19.5%, resulting in a total of €2,719 million.

- The operating margin this year decreased to 10.5% from 12.4% in 2024.

- The automotive segment generated revenue of €14,306 million, representing a 2.5% decline from the previous year.

- The Road Transportation segment experienced a severe decline in sales, with sales dropping by 8.7%, while its margin decreased to 4.7%.

- The Specialities segment maintained the highest margin at 13.5% despite a 4.5% decrease in sales.

- North America sales declined 9.1%, the largest decrease among all regions.

- The company reduced its workforce to 122,600 employees, a 5.5% decrease from the previous year.

- The company saw its employee benefit expenses decrease by €131 million, which brought total costs to €7,491 million.

- The company saw its net income decrease by 12%, bringing total earnings to €1,664 million and resulting in a profit margin decline to 6.4%.

- Free cash flow before M&A decreased to €2,126 million, representing a 4.4% reduction.

- The company reduced its capital expenditure by 9.9%, resulting in a total of €1,967 million, as it adopted stricter rules for investment spending.

Michelin Sales Performance 2025

(Source: agngnconpm.cloudimg.io)

- Michelin’s 2025 sales report demonstrates how pricing power mitigated the revenue decline driven by higher sales volume.

- The total group sales reached €25,992 million, a decrease of €1,201 million (-4.4%) from the previous year, indicating reduced demand across major markets.

- The primary drag came from volumes, which declined by €1,289 million (-4.7%), underscoring weak automotive demand and slower transportation activity.

- The company maintained its pricing power and premium product positioning through a positive price-mix effect, which generated €827 million in revenue.

- The third quarter of 2025 saw its most significant year-over-year decrease, at -6.6%.

- The first quarter of 2025 saw a moderate decline of 1.9%, indicating that the situation began to stabilize at the beginning of the year.

- Currency fluctuations created a major burden, resulting in a negative effect of €817 million, or -3.0%, demonstrating that the company faced foreign exchange challenges throughout its international operations.

- The non-tire product sales increased by 0.3%, while the consolidation scope remained unchanged, indicating that business activities through acquisitions and divestitures had minimal impact.

Michelin Segment Performance 2025

(Source: agngnconpm.cloudimg.io)

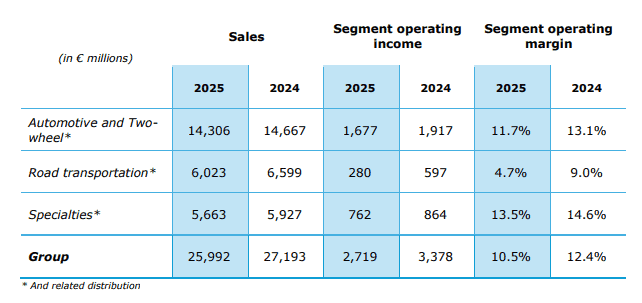

- The 2025 performance of Michelin’s segments demonstrates how difficult macroeconomic conditions have led to decreases in both sales and segment operating income and profit margins.

- The total group revenue reached €25,992 million in 2025, down from €27,193 million in 2024, representing a 4.4% contraction.

- Segment operating income declined 19.5% to €2,719 million, while the operating margin fell from 12.4% to 10.5% due to rising expenses and declining customer demand.

- The Automotive and Two-Wheel segment, the company’s core revenue driver, generated €14,306 million, down 2.5% YoY, with margins narrowing to 11.7% from 13.1%.

- The Road Transportation segment showed its steepest decline, with sales down 8.7% to €6,023 million and operating income down more than 50% to €280 million, leading to a significant margin decline to 4.7%.

- The Specialities segment demonstrates its ability to withstand challenges, achieving €5,663 million in sales with a 4.5% YoY decrease while maintaining a 13.5% operating margin, the highest among all segments.

- The data reveals three main findings about Michelin’s business operations, which include margin compression, segment divergence, and cyclical demand challenges, whereas the company depends on its high-margin speciality business to counteract the decline in transportation-related business operations.

Michelin Regional Sales Breakdown 2025

(Source: agngnconpm.cloudimg.io)

- Michelin reports its 2025 regional sales results, which show that international markets do not have uniform demand patterns and that North America is the main obstacle to revenue expansion.

- The group’s total sales reached €25,992 million, a 4.4% decrease from the previous year, due to varying market conditions across regions.

- Michelin operates its most extensive business in Europe, which generates €9,632 million or 37.1% of total revenue while showing a small 1.5% YoY revenue decrease.

- France contributed €2,559 million to European sales, accounting for 9.8% of total sales, indicating that domestic demand remained stable.

- The most significant decrease in business performance occurred in North America, which includes Mexico, where sales dropped 9.1% YoY to €9,543 million, reducing its revenue contribution to 36.7%. The region shows a decline because automotive demand wanes and fleet operations decrease, while economic challenges affect the area.

- The emerging markets show stable conditions, with other regions producing €6,818 million, accounting for 26.2% of total sales and showing a 1.5% sales decrease.

- The first half of the year generated sales of €13,028 million, while the second half produced €12,965 million in sales, indicating a slight decrease. The demand situation will remain weak throughout the upcoming year of 2025.

Michelin Workforce Costs and Efficiency Trends 2025

(Source: agngnconpm.cloudimg.io)

- Michelin’s 2025 workforce data shows that the company intends to achieve cost savings, better productivity, and improved operational performance through its current economic challenges.

- Total employee benefit costs declined to €7,491 million, down €131 million (-1.7% year-over-year) from €7,622 million in 2024.

- The organization faced margin pressure because its total sales costs increased to 28.8%, which resulted from decreased revenue and not because of higher labor expenses.

- The organization demonstrates operational efficiency through its employment pattern developments. The number of employees on payroll fell to 122,600, a 5.5% decrease, while full-time equivalent (FTE) employees declined to 115,800 (-6.2%).

- The average FTE workforce also dropped by 4.0% to 119,800, signaling ongoing workforce rationalization and restructuring efforts.

- The labor cost-to-sales ratio increased despite the organization achieving cost reductions because top-line revenue declines exceeded the financial benefits from cost reductions, which directly affected profitability.

- Michelin seeks to maintain its profit margins through workforce reduction,s which it balances against efficiency improvements in response to weak market demand.

Michelin Cost Strategy Analysis 2025

(Source: agngnconpm.cloudimg.io)

- The cost structure of Michelin for the year 2025 establishes equitable distribution between expense management and the funding of essential strategic initiatives, which include sales and marketing and research and development (R&D) activities.

- The sales and marketing expenses reduced to €1,176 million, which represents a €28 million decrease that equals a 2.4 % drop from the previous year because the expenses reached €1,204 million in 2024.

- The expenses reached 4.5 % of total sales, which represents a minor increase from 4.4 % because revenue decreased instead of the company implementing aggressive cost reductions.

- Michelin continues to use its planned marketing budget, which helps the company establish its brand identity while reaching customers and generating market demand, even though the market shows weaker performance.

- R&D expenses grew to €788 million, which represents a 0.2 % annual increase that corresponds to 3.0% of sales.

- The decrease in marketing expenditures, together with persistent R&D funding, demonstrates that the organization has shifted its focus towards developing long-term innovative solutions instead of spending on immediate advertising.

- Michelin focuses on building technological dominance, which will create future growth opportunities while the company controls its operational expenses.

Michelin Net Income and EPS Trends in 2025

(Source: agngnconpm.cloudimg.io)

- Michelin shows a small decrease in its 2025 profitability metrics, indicating ongoing margin pressures, although its operational performance remains unchanged.

- The company reported net income of €1,664 million, down from €1,890 million in 2024, reflecting a €226 million decline (-12%).

- The net profit margin decreased from 7.0% to 6.4% due to rising operational expenses and emerging economic challenges.

- A deeper look at earnings per share (EPS) reveals similar trends. Basic EPS fell to €2.36 from €2.65, while diluted EPS declined to €2.33, both representing a ~11% contraction. The decrease shows that shareholders received less value, which acts as an essential financial performance metric that investors monitor.

- The decrease in shareholders’ income reached €220 million, reinforcing the trend of declining profitability.

- The non-controlling interests showed a slight negative shift, indicating that minor structural changes occurred.

Michelin Investment Strategy Insights

(Source: agngnconpm.cloudimg.io)

- Michelin shows its capital expenditure plan through disciplined spending, which enables the company to finance its growth needs while maintaining responsible financial management.

- The company reported gross capital expenditure (CapEx) of €1,967 million, down from €2,182 million in 2024, marking a €215 million decline (-9.9%).

- The company reduced its capital expenditures (CapEx) to 7.6% of revenue from 8.0% previously, indicating it implemented stricter investment regulations amid changing market conditions.

- The financial statement reveals that organizations spent €1,880 million on acquiring new intangible and physical assets, including property and equipment.

- The organization spent €2,215 million in 2024. The company experienced a decrease of €335 million, which represents a 15.1% drop from its earlier expenses.

- The organization achieved €137 million in asset sales, resulting in a negative cash outflow exceeding the previous year’s total of €35 million. This demonstrates that the organization actively manages its portfolio through the sale of non-essential assets.

- The investment grants and payable adjustments decreased to €50 million. This demonstrates that the organization received less financial assistance from outside sources.

Michelin Free Cash Flow

(Source: agngnconpm.cloudimg.io)

- The free cash flow performance that Michelin demonstrates in 2025 shows both strength and strategic investment balance of its operations.

- The company generated €3,819 million in net cash from operating activities, a decline of €517 million (-11.9%) from €4,336 million in 2024, driven by lower operating inflows amid macroeconomic challenges.

- The company spent €778 million on regular capital expenses, down from €951 million previously.

- The expenses on competitiveness and growth projects reached €986 million, which resulted in a total decrease of €224 million from standard capital expenditure because the organization aimed to maintain capital spending control and reduce costs.

- The company increased its expenditures on new business development to €204 million, demonstrating its dedication to ongoing innovation.

- Cash flow performance was significantly impacted because “other cash flow items” increased to €273 million, representing a 285% rise.

- The company reported free cash flow of €2,126 million before mergers and acquisitions, which represents a small decrease of €99 million (-4.4%).

- The FCF after M&A reached €2,181 million, including €56 million in merger and acquisition spending.

- The total amount decreased by €44 million from the previous year, representing a decline of 2.0%.

Michelin 2026 Strategic Outlook

- Michelin begins 2026 with a cautiously positive assessment, linking its economic growth plans to the economic disarray in the current environment.

- The tyre market shows stable demand, according to forecasts, which indicate that global trade patterns will fluctuate throughout the period until H1 2026, when business-to-business Original Equipment (OE) markets will begin their cyclical upturn.

- Michelin is pursuing its main strategic change through diversification, enabling the company to grow its Polymer Composite Solutions business, which will launch as a new reporting segment beginning in Q1 2026.

- The company develops high-margin advanced materials production capabilities and non-tire revenue streams, strengthening its business resilience and generating multiple income sources.

- Michelin sets its financial objectives to achieve annual increases in segment operating income (iso-forex, iso-scope) and to generate more than €1.6 billion in free cash flow before M&A, demonstrating its ability to generate cash flow and use capital effectively.

- Michelin acquired Cooley Group in January 2026, expanding its industrial materials business.

- The company plans to acquire Flexitallic in H1 2026, which will elevate its status as a leader in sealing technologies across the energy and chemical industries.

Michelin Corporate Strategy 2025–2026

- Michelin implements its corporate strategy through multiple business operations, including acquiring companies and funding innovation, while maximizing returns for shareholders.

- The planned acquisitions of Cooley Group and Tex Tech Industries will increase Polymer Composite Solutions’ revenues by 20%, supporting Michelin’s strategy to develop high-margin advanced materials under its Michelin in Motion 2030 plans.

- The company executed a share buyback program, resulting in the cancellation of 22.9 million shares, representing 3.23% of its total share capital.

- The Michelin Innovation Park – Cataroux project, which occupies 42 hectares, demonstrates the company’s dedication to building sustainable innovation ecosystems that support research and development excellence through its 6000 research staff.

- The BIB’Action 2025 plan achieved a 51% employee participation rate among 115,000 employees across 44 countries, resulting in a stronger ownership culture and better internal alignment.

- The company continues to optimize its portfolio by divesting its low-margin, tyre-bias business, allowing it to focus on premium and high-value market segments.

- The “A / A2” credit ratings from Moody’s and Scope Ratings prove Michelin maintains financial stability, which creates confidence among investors.

Michelin M&A and Investment Strategy

- Michelin’s 2024-2025 transaction activity demonstrates its commitment to three core strategic objectives: pursuing specific acquisitions, improving its existing business operations, and developing new high-potential market segments.

- The Group maintained its existing consolidation boundaries in 2025, making no major changes other than the transactions previously announced.

- Michelin conducted several smaller acquisitions with a total value of €51 million, generating direct business results of €29 million in revenue and €2 million in segment operating income, demonstrating Michelin’s strategy of acquiring companies for controlled growth through incremental business development.

- The company made its most significant acquisition in 2024 when it purchased Flex Composite Group for a total enterprise value of €700 million.

- Michelin acquired this deal to strengthen its position in polymer composite solutions and advanced materials markets, as it fits its long-term business expansion plan.

- The completed purchase price allocation process resulted in goodwill of €327 million, demonstrating the company’s strong expectations regarding future operational advantages, technology development, and intangible asset performance.

- The company held essential intangible assets, including €310 million in customer relationships and €39 million in trademarks, demonstrating the strategic value of brand equity and client networks.

- Michelin sold its AddUp stake in October 2024 to implement a portfolio rationalization, including divesting underperforming and non-essential business activities.

Michelin Share Buyback Program

- The share buyback program from Michelin, which will operate between 2024 and 2026, demonstrates their systematized method for managing funds and distributing profits while maintaining their company ownership balance.

- The Group announced a €1 billion multi-year buyback plan, which supports its goal to increase earnings per share (EPS) and deliver value to investors over time.

- Michelin completed €665 million in share repurchases through three agreements, which took place in 2025.

- The first tranche, which commenced in July 2025, included €265 million for purchasing 8.6 million shares at an average cost of €30.80 per share.

- The company entered into two more agreements during October 2025, which totalled €400 million and acquired 14.3 million shares at an average cost of €27.94, which demonstrates their strategy to purchase shares during times of market volatility.

- The company repurchased 22.9 million shares, which it later cancelled in December 2025, therefore decreasing its total outstanding share count.

- The cancellation procedure generates direct benefits for EPS growth and return on equity (ROE) improvements and enhanced capital structure performance.

Sustainability & ESG Metrics: The “Michelin in Motion” Progress

| ESG Metric | 2021 Baseline | 2022 | 2023 | 2024 Actual | 2030 Target | 2050 Ambition |

| Renewable/recycled materials in tyres (ASMR) | 29%. | 30%. | 28%. | 31%. | 40% (all products). | 100% |

| Scope 1 & 2 CO₂ emissions vs. 2019 | –5% (est.) | –20%. | –28%. | –37%. | –47% vs. 2019. | Net zero. |

| Renewable electricity share | Not disclosed | Not disclosed | 54%. | 62%. | Increase ongoing | 100% renewable energy |

| Product energy efficiency (Scope 3 tyre use) vs. 2020 | Baseline | +1.8%. | +2.9% | +4.3%. | +10%. | Full lifecycle net zero |

| Motorsport tyre sustainable content | ~30% (2023 WEC range). | 45% (prototype, road‑approved). | 53% (H24 racing). | 50% (2026 WEC Pilot Sport Endurance announced). | 50%+ mass volume | 100% sustainable racing tires |

| SBTi validation status | Not yet validated | Submitted | Submitted | Approved June 2024 (1.5°C pathway). | Milestone confirmed | Net Zero Standard |

Conclusion

The macroeconomic climate that Michelin faces in 2025. The company experiences decreased revenue and profit. The company maintained its strength through effective pricing methods and expense management. The company displays its dedication to innovation through its research and development investments and its controlled investment of capital resources.

Michelin intends to achieve gradual recovery with improved profit margins through its investment in advanced materials and non-tire business operations, which it will strengthen with acquisitions and operational enhancements.

FAQ

Michelin reported total sales of €25,992 million in 202,5 which represented a 4.4% decrease from the previous year.

Revenue dropped because of decreased sales volume, weak automotive demand and unfavorable currency exchange rates.

The Specialities segment achieved the highest operating margin of 13.5%, which made it the top performer.

Net income decreased to €1,664 million, which represented a 12% decline, while profit margins fell to 6.4%.

Michelin plans to expand its business through advanced materials and premium products while maintaining cash flow through strategic investment.