Alcoa (NYSE: AA) reported Q1 2026 adjusted EPS of $1.40, missing the consensus estimate of $1.47, while revenue of $3.19 billion fell short of the $3.3 billion forecast. Despite the dual miss, shares ticked up 0.47% in after-hours trading to $70.71 on optimism around a stronger Q2 outlook.

About Alcoa Corporation

Alcoa Corporation (NYSE: AA; ASX: AAI) is a global industry leader in bauxite mining, alumina refining, and aluminum production, operating in Australia, Brazil, Canada, Iceland, Norway, Spain, the United States, and other international markets. Founded in 1886 and headquartered in Pittsburgh, Pennsylvania, the company operates through two primary segments: Alumina and Aluminum. In 2025, Alcoa recorded nearly $13 billion in full-year revenue, operating 5 bauxite mines, 5 alumina refineries, and 11 smelting facilities with approximately 13,900 employees.

As of Q1 2026, Alcoa’s market capitalization stood at approximately $18.58 billion, with a trailing P/E ratio of 9.73 and a dividend yield of 0.75%. The company runs on 86% renewable energy across its smelting operations, a key competitive differentiator in the decarbonizing metals sector. A forward annual dividend of $0.40 per share is in place, reflecting disciplined capital return to shareholders.

Top Financial Highlights

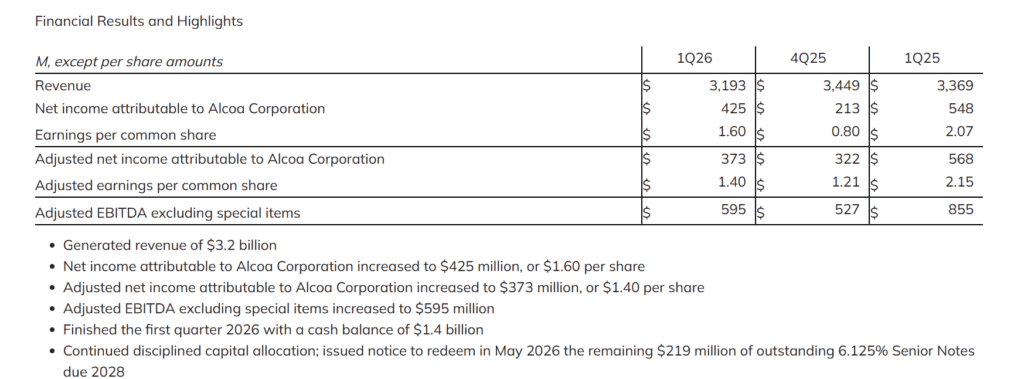

- Total Revenue of $3,193 million ($3.2 billion), a 7% sequential decline from $3,449 million in Q4 2025

- Net Income attributable to Alcoa rose to $425 million, up from $213 million in the prior quarter

- GAAP EPS of $1.60 per diluted share, compared to $0.80 in Q4 2025

- Adjusted Net Income of $373 million, or $1.40 per share, after excluding $52 million in net special items

- Adjusted EBITDA (excluding special items) increased to $595 million, up $68 million sequentially from $527 million in Q4 2025

- Aluminum Segment third-party revenue rose 3% sequentially to $2,536 million, driven by higher average realized price of $4,209/metric ton

- Alumina Segment third-party revenue (alumina + bauxite) fell 33% sequentially to approximately $657 million ($533 million alumina + $124 million bauxite), due to lower shipments and pricing

- Cash balance ended at $1.4 billion, with cash used for operations of $(179) million

- Capital expenditures of $119 million in the quarter; annual capex guidance unchanged

- Free Cash Flow of $(298) million, driven by seasonal working capital build-up

- Return on Equity of 21.9% for the quarter

- Notice issued to redeem remaining $219 million of 6.125% Senior Notes due 2028 in May 2026, using cash on hand

- San Ciprián, Spain smelter restart safely completed in April 2026

- 2026 full-year Alumina production guidance maintained at 9.7 to 9.9 million metric tons; Aluminum at 2.4 to 2.6 million metric tons

Beat or Miss?

| Metric | Reported | Estimate | Difference/Analysis |

| Revenue | $3.19B | $3.30B | Miss by ~$110M; alumina shipment delays from Middle East conflict and Cyclone Narelle |

| Adjusted EPS | $1.40 | $1.47 | Miss by $0.07; shipment volume timing impact expected to reverse in Q2 |

| GAAP EPS | $1.60 | N/A | Beat prior quarter ($0.80) significantly on non-recurring Ma’aden mark-to-market gain |

| Adjusted EBITDA | $595M | $527M (Q4 prior) | Exceeded prior quarter by $68M, driven by higher aluminum prices |

| Cash Balance | $1.4B | N/A | Solid; company executing planned note redemption in May 2026 |

| Alumina Shipments | 1,611 kmt | ~2,105 kmt (Q1 2025 level) | Down 31% sequentially on shipping delays, externally sourced alumina reduction |

| Aluminum Shipments | 613 kmt | ~667 kmt (Q4 2025 level) | Down 8% sequentially due to inventory repositioning and reduced trading |

What Leadership Is Saying?

CEO Quote William F. Oplinger, President and CEO:

“Our experienced team performed very well managing the impacts from the Middle East conflict and Cyclone Narelle. We delivered a solid quarter excluding shipment timing impacts, which we expect to realize in the second quarter of 2026.” On the earnings call, Oplinger added that performance was “driven by execution,” and that Alcoa was “well-positioned to deliver a strong second quarter and full year 2026 performance.”

CFO Quote Molly S. Beerman, Executive Vice President and CFO:

Beerman detailed the Q1 results on the earnings call, noting that adjusted EBITDA of $595 million was driven primarily by higher LME and Midwest premium aluminum prices. At a prior JPMorgan conference, Beerman had signaled strategic positioning: “We have a strong start to 2026. We’re operating stably. We’re progressing our strategic initiatives, and we are really looking to capitalize on the high metal prices and dropping that profitability to the bottom line.”

Historical Performance

Alcoa YoY Comparison

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $3,193M | $3,369M | -5.20% |

| Net Income (attributable to Alcoa) | $425M | $548M | -22.40% |

| Adjusted EPS | $1.40 | $2.15 | -34.90% |

| Adjusted EBITDA | $595M | $855M | -30.40% |

| GAAP EPS | $1.60 | $2.07 | -22.70% |

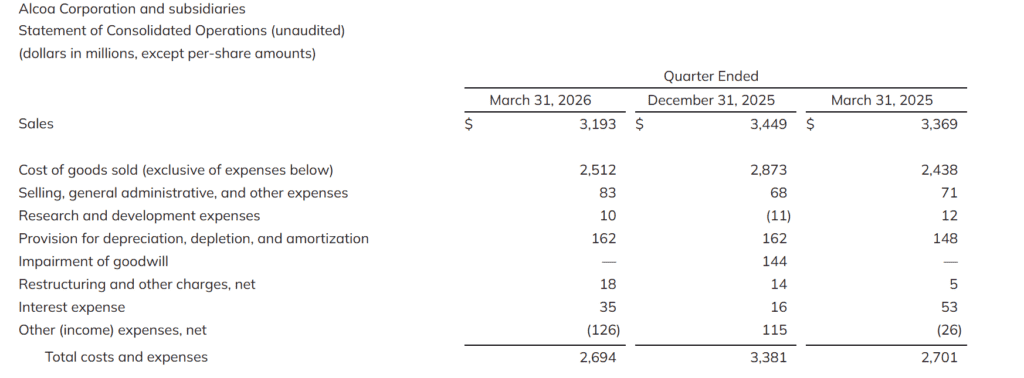

| Cost of Goods Sold | $2,512M | $2,438M | 3.00% |

| Cash from Operations | $(179)M | $75M | N/M (swing to negative) |

| Alumina Avg. Realized Price/ton | $324 | $575 | -43.70% |

| Aluminum Avg. Realized Price/ton | $4,209 | $3,213 | 31.00% |

The dramatic decline in adjusted EBITDA year-over-year reflects the collapse in alumina prices: average realized third-party alumina price fell from $575/ton in Q1 2025 to $324/ton in Q1 2026, a drop of 43.7%. This was partially offset by a 31% rise in average realized aluminum prices ($4,209/ton vs $3,213/ton), driven by higher LME aluminum and Midwest premiums.

Competitor Comparison

Aluminum Sector YoY Performance

| Category | Alcoa Q1 2026 | Alcoa Q1 2025 | Change (%) |

| Revenue | $3,193M | $3,369M | -5.20% |

| Net Income | $425M | $548M | -22.40% |

| Adjusted EBITDA | $595M | $855M | -30.40% |

| Category | Rio Tinto FY 2025 | Rio Tinto FY 2024 | Change (%) |

| Total Revenue | $57.6B | ~$53.6B | +7% |

| Underlying Earnings | $10.9B | $10.9B | Flat |

| Aluminium EBITDA | $4.6B | $3.6B | +28% |

| Operating Cash Flow | $16.8B | $15.6B | +8% |

| Category | Norsk Hydro FY 2025 | Norsk Hydro FY 2024 | Change (%) |

| Revenue (NOK) | 207,971M | 203,636M | +2.1%simplywall |

| Net Earnings (NOK) | 6,717M | 5,790M | +16%simplywall |

| Q4 2025 Adjusted EBITDA | NOK 5.6B | NOK 7.7B | -27%quartr |

How the Market Reacted?

Despite missing both EPS and revenue consensus estimates, Alcoa shares rose 0.47% in after-hours trading on April 16, 2026, reaching $70.71. Investors appeared to look past the headline misses, focusing instead on the sequential jump in net income (from $213 million to $425 million), the higher adjusted EBITDA, and the favorable Q2 2026 guidance that calls for approximately $55 million in sequential aluminum segment EBITDA improvements.

The alumina shipment shortfall was widely attributed to temporary factors: the ongoing Middle East conflict disrupting Australian shipping lanes and the impact of Cyclone Narelle, both of which are expected to normalize in Q2. During regular trading on April 16, the stock closed at $70.81, and broader sentiment tilted bullish given the strong aluminum price tailwind and San Ciprián smelter restart completion.