Market Size, CAGR, and What’s Fueling Growth?

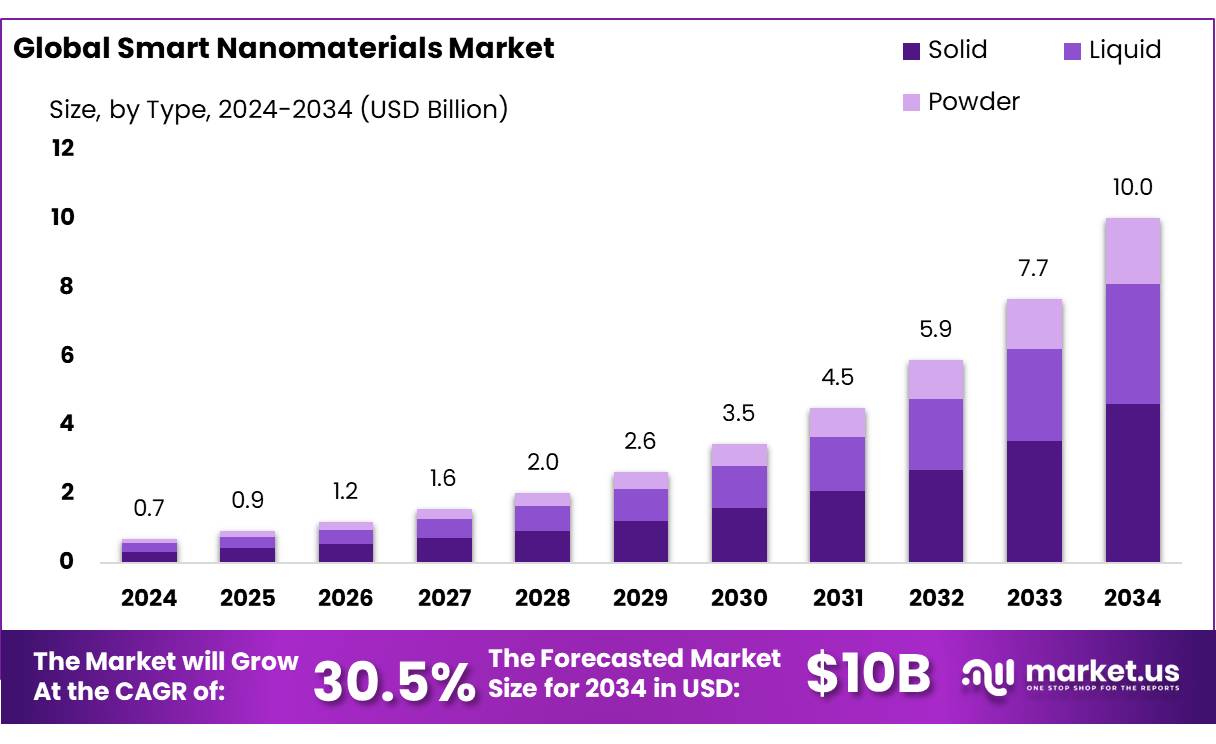

The global Smart Nanomaterials Market is projected to grow from USD 0.6 billion in 2024 to around USD 10.0 billion by 2034, registering a CAGR of 30.5% over the forecast period. This explosive expansion is driven primarily by accelerating adoption in healthcare, display technologies, and nanocoatings, supported by strong R&D pipelines and demand for high‑performance, multifunctional materials across advanced manufacturing, electronics, and energy applications.

Market Overview

According to Market.us, the smart nanomaterials market is transitioning from niche applications to a critical enabling technology across multiple high‑growth industries, underpinned by the rapid commercialization of nano‑enabled products and strong investment in next‑generation materials science. In 2024, the market is valued at USD 0.6 billion and is forecast to reach USD 10.0 billion by 2034, reflecting a robust 30.5% CAGR, as manufacturers seek materials with superior mechanical strength, conductivity, responsiveness, and self‑healing characteristics. Solid‑form smart nanomaterials account for more than 46.6% of global revenue, underscoring the importance of durable nanostructured solids for coatings, sensors, and structural components across electronics, healthcare, and energy.

On the demand side, healthcare applications lead with more than 37.3% share, while display technology and nano‑coatings also capture significant portions of the value chain as device makers and industrial users pivot to surfaces and interfaces engineered at the nanoscale. Regionally, North America dominates the global market with over 35.7% share—about USD 0.2 billion in 2024—supported by a strong nanotechnology ecosystem, an advanced manufacturing base, and sustained R&D funding.

Key Numeric Takeaways

- In 2024, the market size was valued at USD 0.6 billion.

- By 2034, the market is expected to reach USD 10.0 billion, showing strong future potential.

- The market is projected to grow at a CAGR of 30.5% during the period from 2024 to 2034.

- Solid smart nanomaterials led by form, accounting for more than 46.6% of the global revenue share.

- Nano-coatings emerged as a key technology segment, capturing over 32.2% share.

- Display technology followed closely, holding more than 31.1% share in the market.

- Healthcare applications dominated the application segment with over 37.3% share.

- In 2024, North America held a leading regional position with more than 35.7% share, valued at around USD 0.2 billion.

Request For Sample Report Here: https://market.us/report/smart-nanomaterials-market/free-sample/

| Report Features | Description |

| Market Value (2024) | USD 0.7 Bn |

| Forecast Revenue (2034) | USD 10.0 Bn |

| CAGR (2025-2034) | 30.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Solid, Liquid, Powder), By Type (Nano-coatings, Nanocomposites, Nanotubes, Nanoparticles, Nanofibers), By Application (Display Technology, Drug Delivery, Coating and nanofilms, Monitoring and Biosensing, Water Treatment, Others), By End Use (Healthcare, Construction, Consumer Goods, Aerospace, Agriculture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M, Advanced Nanotechnology, Applied Nanotech, Arkema, ARRA, BASF, Cnano, DuPont, Elekta, Fiber Lean, Honeywell, Kruger, Mitsui Kinzoku, Nanoco Group, NanoComposix, Nanocyl, Nanopartz, Nanophase Technologies, Nanosys, OCSIAI, Oxford Instruments, Praxair, Raymor, Showa Denko, SigmaAldrich, SkyNano, Sumitomo Metal Mining, Umcor, Zeon Nano Technology |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

Feel Free Reach Analyst at – [email protected]

Segmentation Deep Dive

By Form / Type

The market is commonly segmented by form, with solid smart nanomaterials holding a dominant position, accounting for more than 46.6% of global revenues in 2024. Solid forms—including nano‑structured coatings, films, powders, and composites—are favored because they deliver robust mechanical performance, ease of integration into existing industrial processes, and compatibility with a wide array of applications spanning electronics, aerospace, automotive, and medical devices. Their ability to provide durability, enhanced strength, and tailored conductivity makes them attractive for both structural and functional roles, from scratch‑resistant surfaces to embedded sensing elements in smart components.

By Application

Applications for smart nanomaterials span a wide spectrum, but healthcare, display technology, and nano‑coatings stand out as the most significant current revenue contributors.

Display Technology (≥ 31.1% share): Display technology holds a 31.1%+ share, leveraging smart nanomaterials to enhance brightness, contrast, energy efficiency, and flexibility in next‑generation screens. Nano‑structured layers and quantum‑scale materials enable thinner, lighter, and more power‑efficient displays for smartphones, TVs, augmented reality devices, and automotive cockpits.

These application clusters benefit from converging trends: miniaturization, demand for smart and connected devices, stricter performance and durability requirements, and an increased focus on hygiene and sustainability.

By End‑User

End‑user industries adopting smart nanomaterials include healthcare, electronics and semiconductors, automotive and aerospace, energy and environment, and construction and infrastructure.

Healthcare end‑users, capturing more than a 37.3% due to the sector’s willingness to invest in high‑value materials that can improve patient outcomes, enable new therapies, and meet stringent regulatory and performance standards. Hospitals, medical device manufacturers, and pharmaceutical companies are key customers for nano‑engineered coatings, implants, diagnostic tools, and drug‑delivery systems.

Regional Analysis

Why North America Leads?

North America is the leading region in the global smart nanomaterials market, capturing more than35.7% of revenues in 2024, equivalent to approximately USD 0.2 billion. The region’s leadership is anchored in a strong R&D ecosystem, extensive government and private‑sector investment in nanotechnology, and the presence of major nanomaterials producers and advanced manufacturing clusters across the United States and Canada. High adoption across electronics, healthcare, automotive, aerospace, and energy further reinforces this position, as end‑users actively deploy nano‑engineered solutions to improve performance, extend service life, and reduce maintenance costs.

Government‑funded nanotech programs, robust IP portfolios, and partnerships between universities, national labs, and industry leaders have created a fertile innovation environment, accelerating the translation of fundamental research into commercial smart nanomaterial products. Additionally, North America benefits from advanced regulatory and standards frameworks that, while stringent, provide clarity and confidence for market participants, supporting faster scale‑up and broader acceptance of nano‑enabled technologies in sensitive sectors such as healthcare and aerospace.

Market Leaders

The smart nanomaterials landscape is highly competitive, with a mix of diversified chemical giants, specialized nanotechnology firms, and advanced materials companies driving innovation and capacity expansion. Key players active in nanomaterials and related smart nano‑enabled solutions include:

- 3M – A leading provider of nano‑engineered films, coatings, and advanced materials for electronics, healthcare, automotive, and energy applications.

- BASF SE – A major chemical company producing high‑performance nanomaterials for coatings, automotive, construction, and industrial applications.

- DuPont – Active in advanced materials and nano‑enabled solutions for electronics, healthcare, and specialty industrial uses.

- Merck Group (Merck KGaA) – Supplies nanomaterials and specialty chemicals for electronics, life sciences, and performance materials.

- Cabot Corporation – Provides conductive and structural nanomaterials (e.g., carbon blacks, specialty carbons) used in energy storage, plastics, and coatings.

- Arkema – Strong in smart self‑healing and functional polymer‑based nanomaterials for automotive, construction, and electronics.

- Nanocyl – Focused on carbon nanotube‑based materials for electronics, energy, and high‑performance composites.

- Showa Denko – Active in advanced nanomaterials for electronics and industrial applications, including carbon‑based and functional materials.

- OCSiAl – A major supplier of single‑wall carbon nanotubes used to enhance mechanical and electrical properties in composites and coatings.

These companies collectively shape technology roadmaps, pricing dynamics, and application development paths within the smart nanomaterials space.

Recent Developments Among Leading Players

Recent strategic moves by key participants underscore the rapid commercialization and portfolio expansion underway in smart nanomaterials and adjacent nano‑enabled markets.

- 3M (2024): In 2024, 3M’s nanomaterial‑based products continued to dominate electronics‑oriented markets, particularly in advanced nanocoatings and films used to improve durability and performance of consumer and industrial devices. The company’s nanomaterial‑related revenues were projected to reach about USD 350 million, reflecting ongoing expansion in automotive and healthcare applications where high‑performance nano‑engineered surfaces and films are in high demand.

- Arkema (2025–2026): Arkema has been expanding its portfolio of smart self‑healing nanomaterials, targeting automotive and structural applications that benefit from autonomous repair of micro‑damage, thereby reducing lifecycle costs and enhancing safety. Industry outlooks for 2025–2034 highlight Arkema as one of the key players driving advances in self‑healing nano‑formulations with recovery efficiencies exceeding 80%, supported by strong patent positions.

- Nanocyl (2025–2026): Nanocyl is reinforcing its position in carbon nanotube‑based smart nanomaterials used in conductive polymers, batteries, and ESD (electrostatic discharge) management. The company is part of a group of leaders that collectively hold around 35% of global smart self‑healing nanomaterials production capacity through advanced formulations and strategic IP.

These developments illustrate a clear pattern: leading players are moving aggressively to secure market share and technological leadership in smart nanomaterials by combining R&D investment, capacity expansion, and targeted application development.

How AI is Reshaping the Future of Smart Nanomaterials?

Artificial intelligence is rapidly becoming a foundational tool for the discovery, design, and deployment of smart nanomaterials, compressing development cycles and unlocking combinations of properties that are extremely difficult to identify using conventional trial‑and‑error R&D.

1. AI‑Driven Materials Discovery and Design

AI and machine learning models are increasingly used to screen vast compositional and structural spaces to identify nanomaterial formulations with targeted properties such as high conductivity, tunable optical behavior, or self‑healing capabilities. For example, major nanomaterials and nanotechnology suppliers like 3M, BASF, DuPont, Merck, and Cabot rely on advanced modeling and data‑driven design workflows to optimize nano‑coatings, conductive fillers, and functional additives for electronics, automotive, and energy systems. By learning from large experimental datasets, AI tools can predict how changes at the nanoscale (particle size, shape, surface functionalization) will influence macroscopic performance, significantly reducing lab iterations and accelerating commercialization.

2. Intelligent Process Control and Quality Assurance

On the manufacturing side, AI‑enabled process control systems monitor parameters such as temperature, particle dispersion, and reaction conditions in real time to keep nanomaterial production within tight quality specifications. According to industry analyses of nanotechnology and nanomaterials production, AI‑enhanced monitoring helps reduce batch variability, increase yields, and ensure consistent performance in downstream applications like nano‑coatings and display materials. Computer vision and sensor fusion algorithms are also being deployed to detect defects and anomalies in nano‑engineered films and coatings, improving reliability for high‑value applications such as flexible displays and medical devices.

Conclusion

A High‑Growth, High‑Impact Investment Theme

The smart nanomaterials market is on track to expand from USD 0.6 billion in 2024 to around USD 10.0 billion by 2034, reflecting a 30.5% CAGR and positioning it as one of the most dynamic segments in the broader advanced materials landscape. Growth is underpinned by structural demand from healthcare, electronics, display technology, and nano‑coatings, alongside robust regional leadership in North America and accelerating adoption in Asia‑Pacific. At the same time, AI‑driven discovery, design, and process optimization are compressing development cycles and enabling smarter, more efficient materials, reinforcing the sector’s innovation intensity and long‑term value creation potential.

For investors, technology strategists, and corporate decision‑makers, smart nanomaterials now represent a strategic cornerstone for next‑generation products and infrastructure combining high growth rates, deep cross‑industry relevance, and a rapidly maturing ecosystem of global leaders actively shaping the market’s future direction.