Introduction

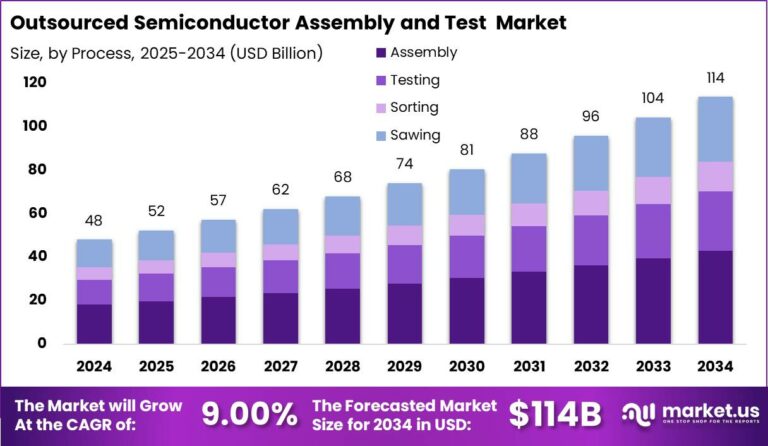

The Outsourced Semiconductor Assembly and Test (OSAT) Market is projected to reach USD 114 Billion by 2034, rising from USD 48.1 Billion in 2024, at a CAGR of 9.00%. Growth is primarily driven by rising semiconductor demand across AI, automotive electronics, and consumer devices, along with increasing fabless chip production and cost optimization strategies.

To learn more about this report request sample @ https://market.us/report/outsourced-semiconductor-assembly-and-test-osat-market/request-sample/

Market Overview

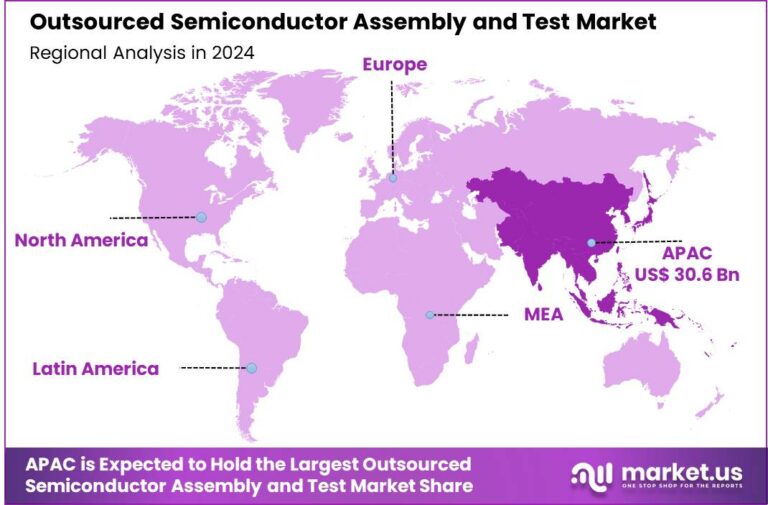

According to Market.us, the global OSAT market is witnessing steady expansion as semiconductor manufacturers increasingly rely on outsourcing to improve efficiency and reduce operational costs. In 2024, Asia-Pacific held a dominant position with over 63.7% share, generating USD 30.6 billion in revenue.

China alone accounted for USD 18.38 billion and is expected to grow at a CAGR of 9.06%, reflecting strong domestic semiconductor demand and government-backed manufacturing initiatives. The market trajectory remains upward due to rising chip complexity, advanced packaging needs, and the expansion of electronics manufacturing ecosystems globally.

The OSAT industry plays a critical role in the semiconductor value chain, handling back-end processes such as packaging, assembly, and testing. With the increasing adoption of technologies like 5G, IoT, and AI-driven applications, semiconductor production volumes are rising significantly, which in turn is strengthening the demand for outsourced assembly and testing services.

Key Takeaways

- Market Size 2024: USD 48.1 Billion

- Forecast Market Size 2034: USD 114 Billion

- CAGR (2025–2034): 9.00%

- Asia-Pacific Market Share: 63.7%

- Asia-Pacific Revenue: USD 30.6 Billion

- China Market Size: USD 18.38 Billion

- China CAGR: 9.06%

Connect with Our Expert Team at [email protected]

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 48.1 Bn |

| Forecast Revenue (2034) | USD 114 Bn |

| CAGR (2025-2034) | 9.00% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Sawing, Sorting, Testing, Assembly), By Packaging Type (Ball Grid Array, Chip Scale Package, Multi-package, Stacked Die, Quad and Dual), By Application (Automotive, Consumer Electronics, Industrial, Telecommunication, Aerospace and Defense, Medical and Healthcare, Logistics and Transportation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ASE Technology Holding Co. Ltd, Amkor Technology Inc., Powertech Technology Inc., ChipMOS Technologies Inc., King Yuan Electronics Co. Ltd, Formosa Advanced Technologies Co. Ltd, Jiangsu Changjiang Electronics Technology Co. Ltd, UTAC Holdings Ltd, Lingsen Precision Industries Ltd, Tongfu Microelectronics Co., Chipbond Technology Corporation, Hana Micron Inc., Integrated Micro-electronics Inc., Tianshui Huatian Technology Co. Ltd, Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Segmentation Deep Dive

By Type

The OSAT market is segmented into assembly services and testing services. Assembly services are expected to maintain a dominant position due to the increasing demand for advanced packaging technologies such as wafer-level packaging and flip-chip packaging. This dominance is driven by the growing need for miniaturization and enhanced performance in electronic devices.

Testing services are also witnessing steady growth as semiconductor designs become more complex. The demand for comprehensive testing solutions is increasing to ensure reliability and performance, particularly in automotive and industrial applications where failure risks must be minimized.

By Application

Consumer electronics remain a leading application segment, supported by the continuous demand for smartphones, laptops, wearables, and smart home devices. The rapid product replacement cycle in this segment is contributing to sustained semiconductor demand.

The automotive segment is emerging as a high-growth area due to the increasing adoption of electric vehicles and advanced driver assistance systems. These technologies require a large number of semiconductor components, which is boosting demand for OSAT services.

Industrial and telecommunications applications are also expanding, driven by automation and 5G infrastructure deployment. These sectors require high-performance and reliable semiconductor solutions, further supporting market growth.

By End-User

Fabless semiconductor companies represent a major end-user segment, as they rely heavily on OSAT providers for back-end processing. The rise of fabless business models is a key factor contributing to the expansion of the OSAT market.

Integrated device manufacturers are also outsourcing a portion of their assembly and testing operations to improve cost efficiency and focus on core competencies. This trend is expected to continue as companies seek to optimize their supply chains.

Regional Analysis

Asia-Pacific continues to lead the OSAT market, accounting for over 63.7% of the global share in 2024. This dominance is driven by the presence of major semiconductor manufacturing hubs in countries such as China, Taiwan, South Korea, and Malaysia. The region benefits from a well-established supply chain, skilled workforce, and strong government support for semiconductor production.

China plays a particularly significant role, with a market size of USD 18.38 billion and strong growth prospects. Government initiatives aimed at achieving semiconductor self-sufficiency are accelerating investments in local OSAT capabilities. Additionally, the increasing demand for consumer electronics and electric vehicles within the region is further strengthening market growth.

Other regions such as North America and Europe are also witnessing growth, supported by rising investments in semiconductor manufacturing and advanced technologies. However, the Asia-Pacific is expected to maintain its leadership due to its cost advantages and large-scale production capabilities.

Market Leaders

The OSAT market is highly competitive, with several key players dominating the landscape:

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- JCET Group Co., Ltd.

- Powertech Technology Inc.

- Tongfu Microelectronics Co., Ltd.

- UTAC Holdings Ltd.

- ChipMOS Technologies Inc.

- King Yuan Electronics Co., Ltd.

- Hana Micron Inc.

- Unisem Group

These companies are focusing on expanding their advanced packaging capabilities and investing in new technologies to strengthen their market positions.

Recent Developments

- In 2024, ASE Technology expanded its advanced packaging facilities to support high-performance computing and AI chip demand.

- Amkor Technology announced new investments in automotive semiconductor packaging solutions to address growing EV demand.

- JCET Group continued to strengthen its global footprint through capacity expansion in Asia.

- Powertech Technology focused on developing next-generation memory packaging solutions to meet increasing data center requirements.

- Tongfu Microelectronics enhanced its collaboration with global semiconductor companies to improve advanced packaging capabilities.

These developments highlight the industry’s focus on innovation, capacity expansion, and strategic partnerships.

How AI is Reshaping the Future of Outsourced Semiconductor Assembly and Test (OSAT) Market?

Artificial intelligence is becoming a key enabler in the transformation of OSAT operations. Companies are increasingly integrating AI into testing and quality control processes to improve yield rates and reduce defects. For instance, advanced inspection systems powered by AI algorithms are capable of detecting microscopic defects in semiconductor packaging, which enhances reliability and reduces failure rates.

AI-driven predictive maintenance is also gaining traction within OSAT facilities. By analyzing equipment performance data in real time, companies can anticipate failures and minimize downtime. This improves operational efficiency and supports high-volume production requirements.

In addition, AI is optimizing chip testing processes. Machine learning models can analyze vast datasets generated during testing to identify patterns and anomalies more quickly than traditional methods. This accelerates time-to-market for semiconductor products, which is critical in fast-evolving sectors like automotive electronics and consumer devices.

Another emerging application is AI-assisted design for advanced packaging technologies such as system-in-package and 3D stacking. These solutions require high precision and complex integration, where AI helps optimize layouts and thermal performance.

Overall, AI is not only improving efficiency but also enabling OSAT providers to handle increasingly complex semiconductor designs, making it a fundamental driver of future market growth.

Conclusion

The OSAT market is positioned for sustained growth, supported by rising semiconductor demand across multiple industries and the increasing complexity of chip designs.

The shift toward outsourcing, combined with advancements in packaging technologies and AI integration, is creating strong opportunities for market participants. Asia-Pacific is expected to remain the dominant region, while global investments in semiconductor manufacturing will continue to drive expansion.

For investors and industry stakeholders, the OSAT market presents a compelling opportunity, driven by long-term technological trends and the growing importance of semiconductors in the global economy.