Edtech Market Size

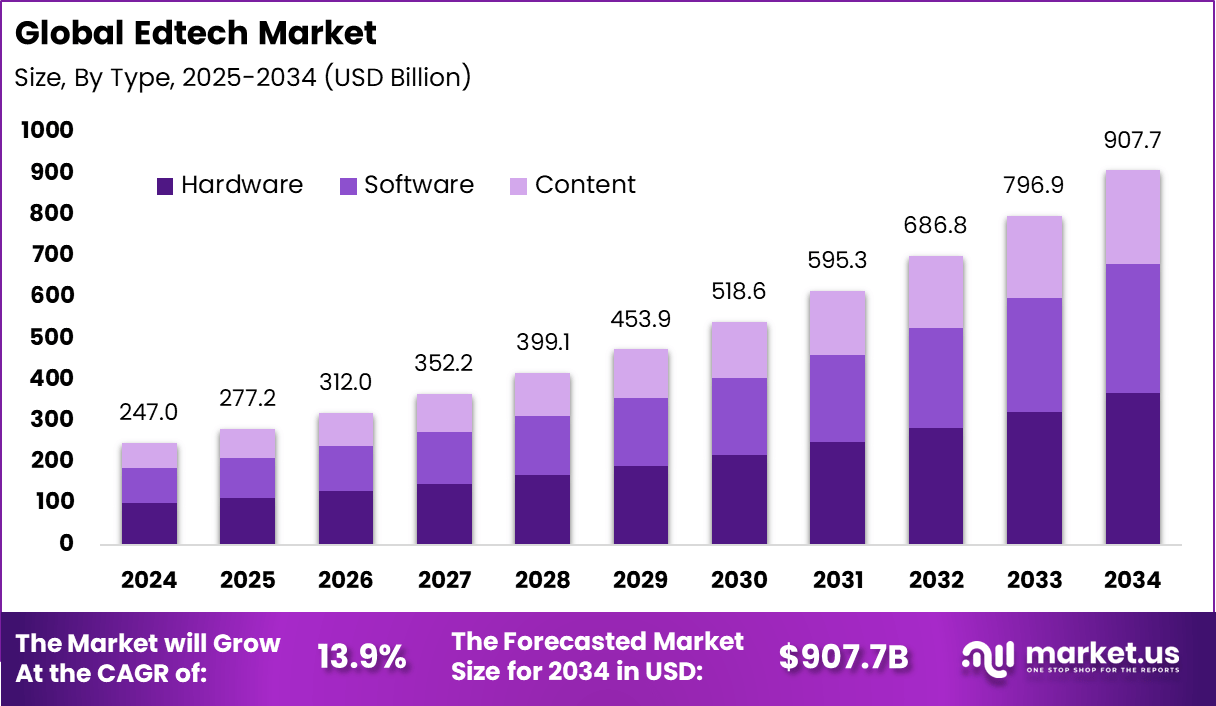

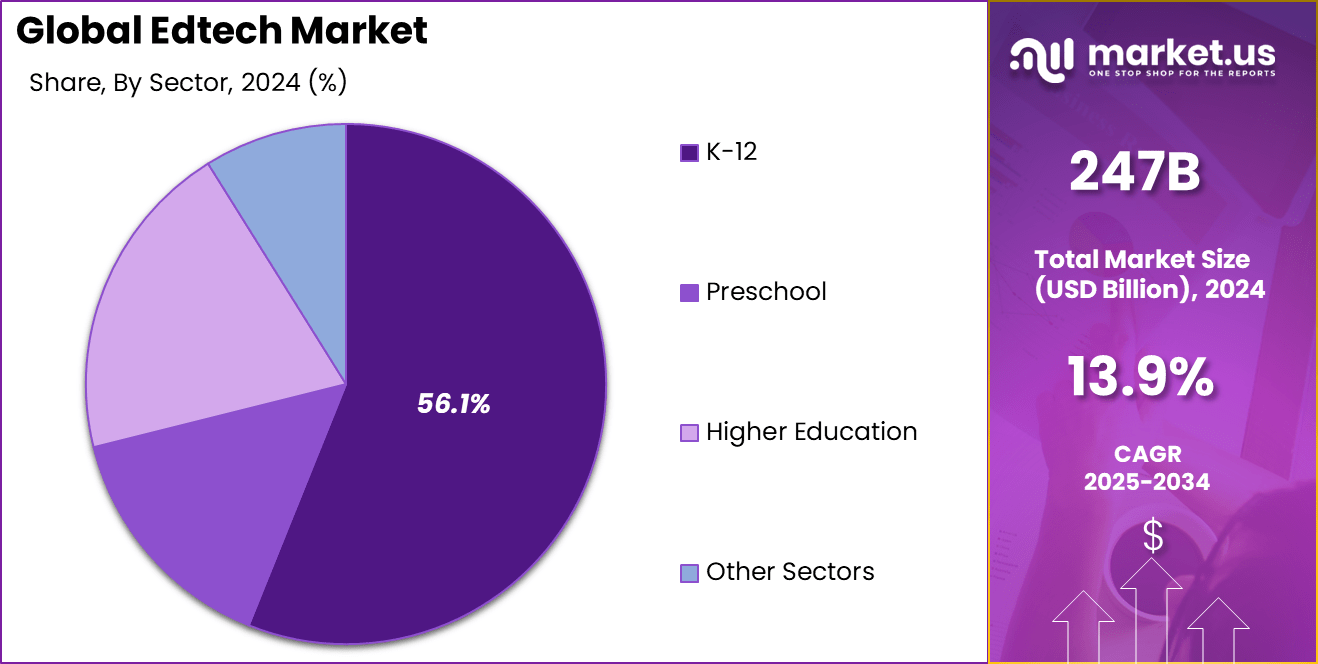

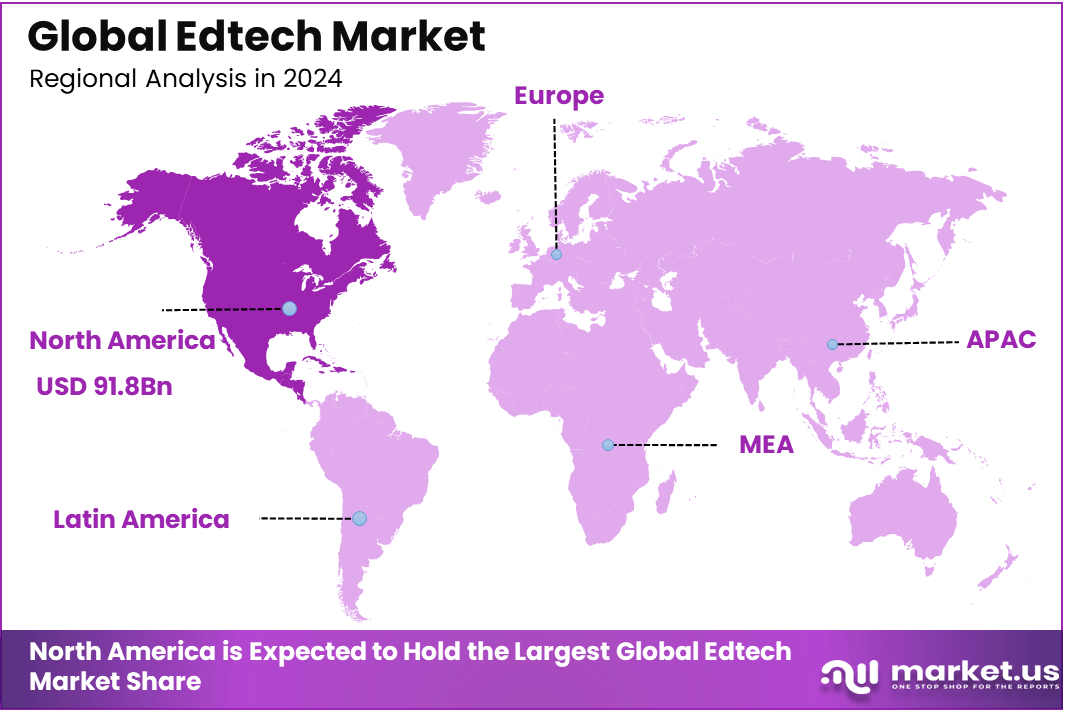

According to Market.us, The global EdTech market reached USD 247 billion in 2024 and is expected to continue expanding, with projections indicating a rise from USD 277.2 billion in 2025 to approximately USD 907.7 billion by 2034, reflecting a compound annual growth rate (CAGR) of 13.9% during the forecast period. In 2024, North America maintained a dominant market position, accounting for over 37.2% of the total market share, generating USD 91.8 billion in revenue.

Top Market Takeaways

- On-premise solutions dominate with 70.3%, driven by institutions’ preference for control and data security.

- Hardware accounts for 40.5%, reflecting strong demand for smart devices and interactive tools in classrooms.

- K-12 sector leads with 56.1%, showing early adoption of digital learning platforms in schools.

- Businesses represent 67.8% of end-users, highlighting corporate investment in training and upskilling through digital learning tools.

- North America holds 37.2% share, supported by mature EdTech ecosystems and strong institutional adoption.

- The U.S. market reached USD 84.14 billion, expanding at a CAGR of 11.7%, reflecting continued investment in digital education infrastructure.

For Proper Guidance for your Business, Invest On Report Here: https://market.us/purchase-report/?report_id=101919

Quick Market Facts

- Cloud deployment is growing from 28.1% in 2019 to 29.4% in 2024, with steady growth.

- On-premise deployment declines slightly from 71.9% to 70.6% over the same period, but remains dominant.

- Hardware is decreasing from 41.5% in 2019 to 40.5% in 2024, while software increases from 27.9% to 29.0%.

- Content remains stable at around 30.6% across the years.

- K-12 grows from 54.2% in 2019 to 56.1% in 2024, maintaining its position as the largest sector.

- Preschool remains stable at 11.3% to 11.4%, while Higher Education declines from 20.0% to 19.2%.

- Business end-users decline from 68.6% in 2019 to 67.8% in 2024, while consumer end-users increase from 31.4% to 32.2%.

- North America share declines from 39.9% in 2019 to 37.2% in 2024, while Asia-Pacific grows from 20.9% to 24.2%.

- Europe also sees a slight decline from 30.2% to 29.4%, and Latin America remains stable around 6%. The Middle East & Africa shows slight growth from 3.0% to 3.2%.

EdTech Statistics

- U.S. students engaging with devices for over 60 minutes per week show improved academic outcomes, indicating the effectiveness of technology in education.

- eLearning enhances information retention rates by 25% to 40%, and 84% of learners report higher engagement with gamified EdTech solutions.

- 61% of HR leaders recognize online credentials as equivalent to traditional qualifications, emphasizing the credibility of online education.

- The EdTech sector is expected to grow at a CAGR of 15% in the coming years.

- Corporate EdTech, valued at $27.5 billion, shows strong demand for professional and continuous education.

- Over 70% of colleges plan to introduce new online undergraduate programs in the next three years, reflecting the ongoing shift to online higher education.

Market Overview

Top driving factors of the EdTech market stem from rising demand for digital and personalised learning experiences, increasing internet penetration, and growth in mobile device usage that make online learning more accessible. Learners and institutions are seeking solutions that allow flexible pacing, customised content delivery, and real‑time feedback to improve learning outcomes. The expansion of hybrid and smart classrooms, along with corporate and professional upskilling initiatives, has reinforced demand across academic and vocational segments. These changes are supported by the heightened focus on continuous learning and the need to adapt to evolving workforce requirements.

Demand analysis for EdTech solutions shows sustained interest from educational institutions, governments, and enterprises as digital transformation becomes a strategic priority. Traditional systems are increasingly supplemented or replaced by digital platforms that facilitate remote access, scalability, and enhanced engagement. In higher education, for example, institutions are investing in student engagement platforms and analytics to overcome fragmentation and enhance teaching effectiveness. Learners are also adopting online and blended learning formats to balance education with work and personal commitments.

The increasing adoption of technologies such as artificial intelligence, machine learning, cloud computing, and data analytics is shaping the EdTech landscape by enabling adaptive learning, predictive insights, and personalised guidance. AI‑driven tools can tailor content to individual needs, analyse performance trends, and streamline administrative processes. Cloud‑based platforms offer scalable infrastructure and seamless updates, while mobile and interactive technologies improve accessibility and engagement. Virtual and augmented reality are further enhancing immersive learning experiences for a range of subjects.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Emerging Trend Analysis

Personalized and Adaptive Learning Technologies

The Edtech market is experiencing a strong shift towards personalized and adaptive learning technologies that tailor instruction to individual learner needs. These solutions use data analytics and artificial intelligence to adjust content delivery based on learner performance and preferences, allowing educational content to align more closely with learning pace and ability.

Adaptive learning tools are increasingly incorporated into digital platforms across K‑12, higher education, and corporate training environments to improve engagement and outcomes. The emphasis on customization reflects broader educational priorities to support diverse learner profiles and reduce barriers to effective learning.

By Deployment Mode

In 2025, on-premise solutions dominated the EdTech market, capturing 70.3% of the share. Educational institutions have a strong preference for on-premise solutions due to the level of control and security they offer.

With concerns around data privacy and compliance regulations, many institutions find it crucial to store sensitive student and institutional data on local servers. On-premise solutions provide the assurance of data sovereignty and greater customization options, which are essential for meeting the unique needs of different educational environments.

| Deployment Mode | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Cloud | 28.10% | 28.40% | 28.60% | 28.90% | 29.20% | 29.40% |

| On-Premise | 71.90% | 71.60% | 71.40% | 71.10% | 70.80% | 70.60% |

This preference is also driven by the desire for complete control over the deployment, management, and integration of digital learning platforms. For educational institutions, particularly those with strict regulatory requirements, on-premise solutions ensure a higher level of security and can be tailored to specific operational needs. As digital education tools become more embedded in institutional operations, on-premise solutions continue to be a popular choice for maintaining security and operational control.

By Type

In 2025, hardware accounted for 40.5% of the EdTech market, driven by the growing demand for smart devices, interactive panels, and connected classroom tools. The increasing integration of technology into classrooms has led to a surge in the need for physical devices that support digital learning experiences.

From interactive whiteboards to student devices and collaboration tools, hardware has become a cornerstone of modern education. These devices enhance engagement, enable real-time collaboration, and provide interactive learning experiences that traditional methods could not.

| Type | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Hardware | 41.50% | 41.30% | 41.10% | 40.90% | 40.70% | 40.50% |

| Software | 27.90% | 28.10% | 28.30% | 28.50% | 28.80% | 29.00% |

| Content | 30.60% | 30.60% | 30.60% | 30.60% | 30.60% | 30.50% |

With the rise of hybrid and remote learning models, the need for reliable and effective hardware solutions has grown. Educational institutions are investing heavily in technology infrastructure to ensure that both in-person and online learners have access to the tools necessary for a productive learning experience. The hardware segment is expected to maintain its strong position as schools and universities continue to adopt advanced educational technologies to improve learning outcomes and student engagement.

By Sector

In 2025, the K-12 sector led the EdTech market, holding a 56.1% share. This dominance highlights the rapid adoption of digital learning platforms in schools, especially as educational institutions seek to integrate technology into their classrooms.

The move towards digital learning in K-12 schools has been accelerated by the need for interactive, personalized, and engaging educational experiences. Digital platforms enable teachers to customize lessons, track student progress, and provide instant feedback, which is driving the growth of this segment.

| Sector | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| K-12 | 54.20% | 54.60% | 55.00% | 55.40% | 55.90% | 56.10% |

| Preschool | 11.30% | 11.30% | 11.30% | 11.30% | 11.30% | 11.40% |

| Higher Education | 20.00% | 19.80% | 19.60% | 19.50% | 19.20% | 19.20% |

| Other Sectors | 14.50% | 14.30% | 14.10% | 13.80% | 13.60% | 13.30% |

The early adoption of digital tools in the K-12 sector is also fueled by government initiatives and funding aimed at enhancing education through technology. As schools continue to invest in digital learning solutions, the K-12 sector is expected to maintain a significant share of the market. The use of learning management systems (LMS), educational apps, and e-learning tools has transformed traditional teaching methods, making learning more accessible and engaging for students of all levels.

By End-User

In 2025, businesses represented 67.8% of the EdTech market, reflecting the growing corporate investment in training and upskilling through digital learning tools. Companies are increasingly turning to digital education solutions to equip their workforce with the skills needed to succeed in a rapidly evolving business environment.

Online training programs, webinars, e-learning platforms, and corporate learning management systems are becoming essential tools for organizations looking to improve employee performance, enhance productivity, and ensure compliance with industry standards.

| End-User | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Business | 68.60% | 68.50% | 68.30% | 68.10% | 67.90% | 67.80% |

| Consumer | 31.40% | 31.50% | 31.70% | 31.90% | 32.10% | 32.20% |

The rise of digital learning tools in the corporate sector is driven by the need for continuous skill development and the growing demand for flexible, accessible learning opportunities. As businesses adapt to new technologies and industry trends, they are increasingly investing in EdTech solutions to provide employees with the training necessary to remain competitive. The business sector’s commitment to workforce development through digital education is a key factor driving the growth of this segment in the market.

Regional Insight

In 2025, North America held a dominant 37.2% share of the EdTech market.

Edtech Market by Regional Analysis (%), 2020-2024

| Region | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| North America | 39.90% | 39.30% | 38.80% | 38.20% | 37.30% | 37.20% |

| Europe | 30.20% | 30.10% | 29.90% | 29.80% | 29.60% | 29.40% |

| Asia-Pacific | 20.90% | 21.60% | 22.30% | 22.90% | 24.10% | 24.20% |

| Latin America | 5.90% | 5.90% | 5.90% | 6.00% | 5.90% | 6.00% |

| Middle East & Africa | 3.00% | 3.00% | 3.10% | 3.20% | 3.10% | 3.20% |

This is attributed to the region’s mature EdTech ecosystem, which includes a high level of institutional adoption and strong investments in digital education infrastructure. Educational institutions in North America have been at the forefront of integrating technology into the learning environment, creating a robust market for EdTech solutions. From K-12 schools to universities and corporate training centers, the demand for innovative digital tools continues to rise.

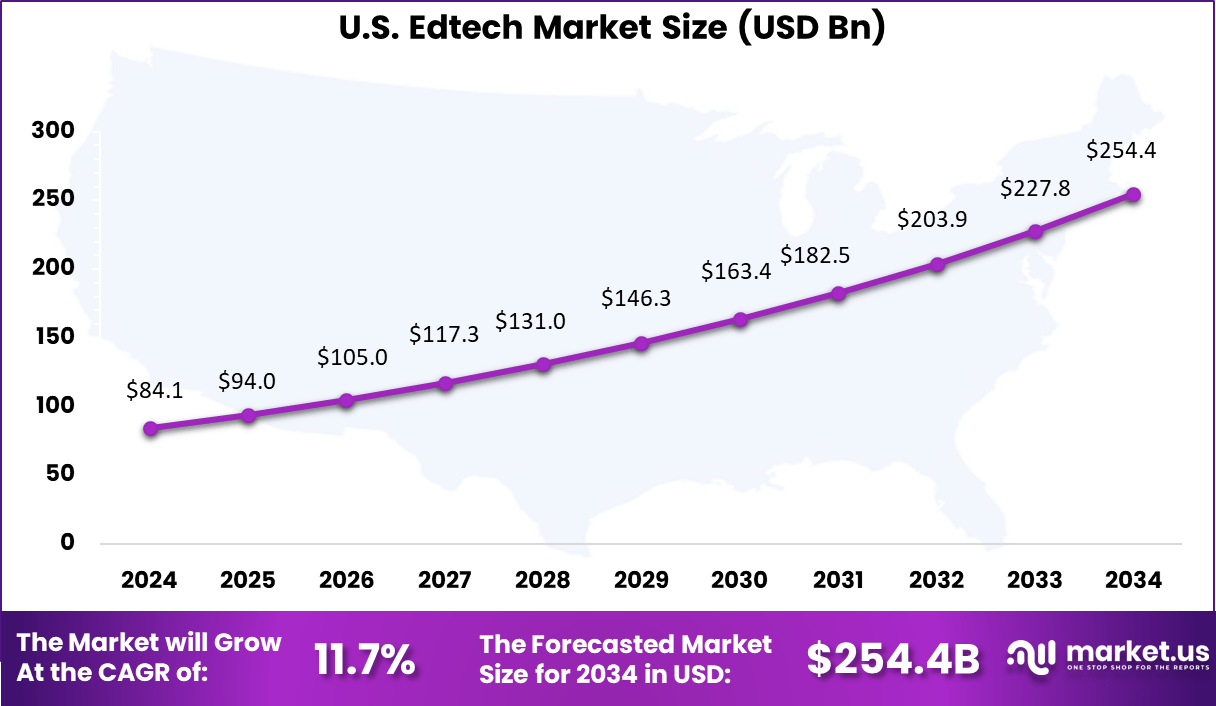

The U.S. market, in particular, reached USD 84.14 billion and is expanding at a steady CAGR of 11.7%. This growth reflects continued investment in digital learning technologies, which are reshaping how education is delivered across various sectors.

With a focus on improving educational outcomes and creating more efficient learning environments, North America remains a leading region in the global EdTech market. The ongoing evolution of learning models, supported by both public and private sector investments, will continue to drive the region’s market dominance.

Drivers Impact Analysis

| Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

| Expansion of Digital Learning Platforms in K 12 and Higher Education | 3.10% | North America, Asia Pacific | Medium to Long Term |

| Corporate Upskilling and Workforce Reskilling Demand | 2.60% | North America, Europe | Short to Medium Term |

| Rising Adoption of AI Based Personalized Learning Tools | 2.10% | Global | Medium Term |

| Growth in Mobile Learning and Affordable Internet Access | 1.70% | Asia Pacific, Latin America | Immediate to Medium Term |

| Government Initiatives Supporting Digital Education | 1.20% | Asia Pacific, Europe | Long Term |

Restraint Impact Analysis

| Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

| Digital Divide and Infrastructure Gaps | -2.40% | Emerging Markets | Medium Term |

| Data Privacy and Student Information Regulations | -1.80% | Europe, North America | Medium Term |

| High Content Development and Platform Costs | -1.30% | Global | Short Term |

| Resistance to Technology Adoption in Traditional Institutions | -0.90% | Europe, Asia Pacific | Medium Term |

| Platform Saturation and Intense Competition | -0.60% | North America | Ongoing |

Key Players Analysis

In the EdTech market, Coursera Inc. and BYJU’S are recognized as global leaders, offering a broad range of online courses and learning platforms for various educational needs. Coursera provides university-backed certifications, while BYJU’S focuses on interactive learning for K-12 and competitive exam preparation. Chegg Inc. and 2U Inc. also play significant roles with their specialized platforms, which offer textbook rentals, online tutoring, and degree programs in partnership with top universities.

Amazon Inc. and Blackboard Inc. have established a strong presence in the market. Amazon’s cloud-based tools support educational institutions, while Blackboard offers learning management systems to enhance virtual classrooms. Edutech and Alphabet Inc. (Google LLC) continue to innovate, with Edutech offering digital solutions and Google supporting educational institutions with its suite of productivity tools and AI technologies. edX Inc. and Instructure, Inc. offer scalable online learning solutions, emphasizing MOOCs and learning management systems.

Udacity, Inc. and upGrad Education Private Limited are key players, focusing on skills development and online certifications, with a particular emphasis on technology and professional courses. These companies, along with other emerging players, are transforming the educational landscape by making learning more accessible, personalized, and scalable. Their solutions cater to learners worldwide, driving the ongoing digital transformation in education.

Top Market Leaders

- Coursera Inc.

- BYJU’S

- Chegg Inc.

- 2U Inc.

- Amazon Inc.

- Blackboard Inc.

- Edutech

- Alphabet Inc. (Google LLC)

- edX Inc.

- Instructure, Inc.

- Udacity, Inc.

- upGrad Education Private Limited

- Other Key Players.

Recent Developments

- January, 2026 – Coursera launched Coursera Coach with agentic AI tutoring. Learners receive real-time feedback across 7,000 courses. Enterprise adoption grew 35% among Fortune 500 firms for compliance training. Google Career Certificates expanded to 150 countries. Mobile app handles 80 million monthly active users. Coursera partners with 300 universities.

- February, 2026 – BYJU’S rolled out BYJU’S Infinity with AR/VR classrooms. K-12 students explore 3D science labs via smartphones. India user base hit 150 million with 40% retention boost. Offline access serves rural markets. Gamified assessments predict exam scores 92% accurately. BYJU’S dominates 60% of Indian edtech.

Conclusion

In conclusion, the EdTech market is experiencing rapid growth driven by technological advancements, the increasing demand for personalised learning experiences, and the shift toward digital transformation across educational and corporate sectors. The integration of artificial intelligence, cloud computing, and data analytics into educational tools is enhancing learning outcomes and operational efficiencies, while also providing new opportunities for scaling education across global and remote environments.

Investment in EdTech is expected to continue expanding, particularly in regions with growing digital infrastructure. As educational institutions and enterprises increasingly recognise the value of digital platforms, the market will likely see continued innovation and expansion, fostering a more accessible, efficient, and adaptive learning ecosystem. However, challenges such as digital accessibility and regulatory compliance must be navigated to ensure equitable and sustainable growth in the sector.