Market Overview

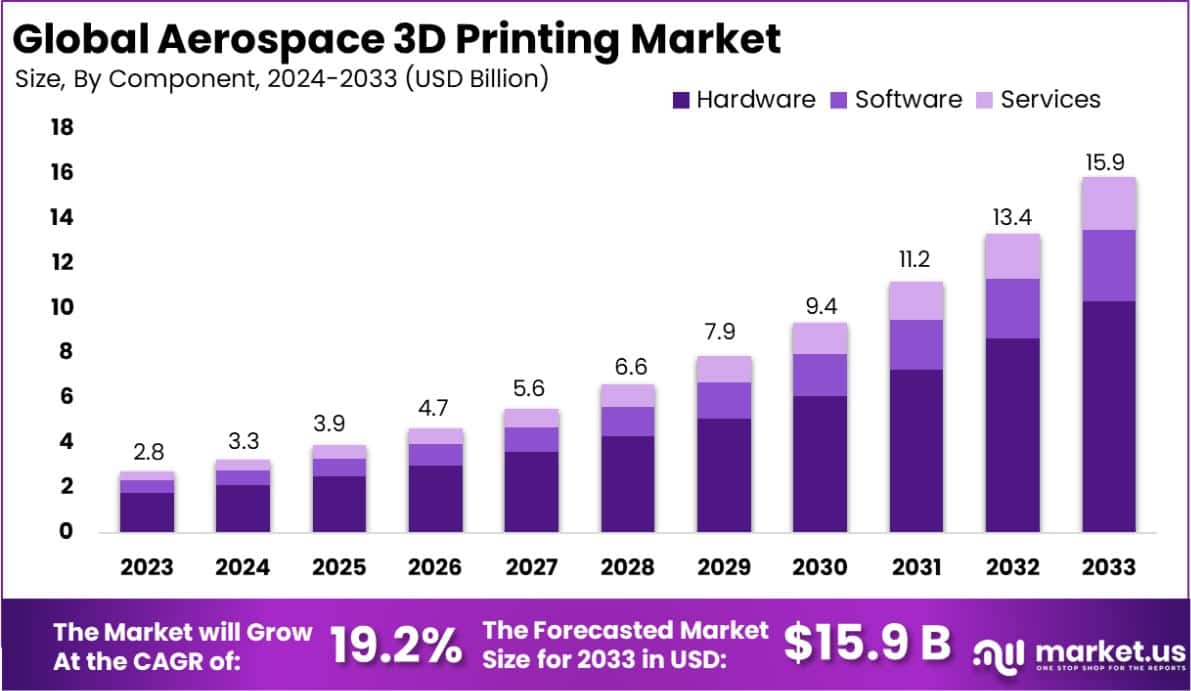

The global aerospace 3D printing market is expanding at a remarkable pace. According to market.us, the market was valued at USD 2.8 billion in 2023 and is projected to reach USD 15.9 billion by 2033. This growth reflects a CAGR of 19.2% over the forecast period from 2024 to 2033, signaling strong long-term demand for additive manufacturing across the aerospace sector.

Aerospace 3D printing, also called additive manufacturing, builds three-dimensional components from digital blueprints by layering material precisely. Airlines and space agencies use this technology to produce lighter, stronger parts at lower cost. Consequently, manufacturers reduce fuel consumption and shorten production timelines compared to traditional fabrication methods.

Demand for lightweight aircraft components drives much of this market growth. Aerospace firms continuously seek ways to cut aircraft weight and improve operational efficiency. Additive manufacturing enables complex structural designs that conventional production cannot replicate, giving engineers greater freedom to optimize components for both performance and durability.

Request a free sample report to explore detailed insights, segmentation data, and regional forecasts: https://market.us/report/aerospace-3d-printing-market/request-sample/

Government investment is also accelerating market momentum. According to hdr.undp.org, the Chinese government earmarked USD 100 million in 2023 to establish a national aerospace additive manufacturing research center. This investment signals strong state-level commitment to building domestic capability and gaining competitive advantage in global aerospace production.

Research funding from other sources further strengthens the industry’s foundation. According to additivemaufacturing.media, nearly USD 12 million in research grants target new materials and process technologies for aerospace applications. These grants help close the gap between laboratory innovation and production-ready solutions, speeding commercialization of next-generation components.

North America currently leads all regions in this market. According to market.us, the region captured a 41% share in 2023, generating USD 1.12 billion in revenue. This leadership reflects the region’s concentration of major aerospace manufacturers, advanced research institutions, and strong private-sector investment in additive manufacturing technology.

Key Takeaways

- The Global Aerospace 3D Printing Market will grow from USD 2.8 billion in 2023 to USD 15.9 billion by 2033, at a CAGR of 19.2%.

- Hardware led the By Component segment in 2023, capturing more than 64.8% of market share.

- Selective Laser Melting (SLM) dominated the By Technology segment in 2023, holding more than 47.5% share.

- Prototyping led the By Application segment in 2023, accounting for more than 54.2% of market share.

- Metal materials led the By Material segment in 2023, capturing more than 58.7% of market share.

- Aircraft dominated the By Platform segment in 2023, holding more than 59.4% of market share.

- North America led all regions in 2023 with a 41% share and USD 1.12 billion in revenue.

Market Segmentation Overview

By Component: Hardware

Hardware captured more than 64.8% of the component segment in 2023, making it the clear market leader. Aerospace firms invest heavily in specialized printing equipment to produce engine parts and structural components. This hardware demand reflects the critical need for precision machinery capable of meeting strict aerospace performance and safety standards.

Software accounted for approximately 22.3% of the segment, supporting design, simulation, and pre-print testing. Advanced software tools reduce material waste and improve component accuracy before production begins. Services contributed the remaining 12.9%, covering on-demand printing, maintenance, and full lifecycle support for aerospace operators.

By Technology: Selective Laser Melting

Selective Laser Melting (SLM) dominated the technology segment with more than 47.5% share in 2023. SLM produces high-density, complex metal structures that meet the precision requirements of turbine blades and aircraft frames. This capability makes it the preferred choice for manufacturing critical aerospace parts that demand both strength and dimensional accuracy.

Electron Beam Melting (EBM) followed with 20.8% share, valued for superior fatigue resistance in high-stress components. Direct Metal Laser Sintering (DMLS) held 16.4%, offering versatility across multiple metal alloys. Stereolithography (SLA) captured 9.3%, favored for detailed prototypes and smooth surface finishes in design validation applications.

By Application: Prototyping

Prototyping led the application segment with more than 54.2% share in 2023. Rapid prototyping shortens design cycles and enables fast iterative improvements in aerospace development. Engineers use printed prototypes to validate performance and ensure compliance with strict safety standards before committing to full-scale production runs.

Tooling accounted for 27.1% of the segment, with 3D printing enabling complex tool designs at lower cost than traditional machining. Functional Parts represented 18.7%, reflecting growing confidence in additive manufacturing processes for delivering finished components that meet rigorous aerospace operational requirements.

By Material: Metal

Metal materials led the segment with more than 58.7% share in 2023. Titanium and aluminum dominate aerospace metal printing due to their lightweight and high-strength properties. These characteristics directly support fuel efficiency and structural integrity targets that aircraft manufacturers must meet to satisfy aviation safety regulations.

Polymers held 24.6% share, primarily used in cabin interiors and non-structural components where weight reduction matters most. Composite materials accounted for 16.7%, offering exceptional strength-to-weight ratios for specialized applications where neither metals nor standard polymers can meet the required performance profile.

By Platform: Aircraft

Aircraft dominated the platform segment with more than 59.4% share in 2023. Additive manufacturing helps aircraft builders reduce component weight, minimize material waste, and shorten production timelines. These advantages translate directly into lower operating costs and improved fuel efficiency across both commercial and military aviation fleets.

Unmanned Surface Vehicles (USVs) captured 22.1% share, benefiting from custom lightweight parts that extend mission endurance. Spacecraft represented 18.5% of the segment, where on-demand part production addresses the practical challenge of carrying spare components on long-duration space missions.

Gain deeper market intelligence before making your next business decision. Request a Free Sample Report

Drivers

Weight reduction goals push aerospace manufacturers toward additive manufacturing solutions. Airlines and defense contractors continuously seek lighter components to lower fuel consumption and extend aircraft range. Aerospace 3D printing enables complex internal geometries that traditional machining cannot produce. Consequently, manufacturers achieve meaningful weight savings without compromising structural strength or component reliability.

Production speed and flexibility also drive adoption of additive manufacturing across the aerospace sector. Aerospace firms use 3D printing to accelerate development cycles and respond faster to design changes. This agility reduces time-to-market for new aircraft programs. Moreover, the technology supports small-batch and custom component production without the high tooling costs that conventional methods require.

Use Cases

Aerospace engineers use 3D printing extensively for rapid prototyping during aircraft design programs. Printed prototypes allow design teams to test and refine components quickly without expensive tooling. This iterative process shortens development timelines significantly. Additionally, rapid prototyping reduces the risk of design errors reaching full-scale production, saving both time and cost for aerospace manufacturers.

Military and commercial aerospace programs use additive manufacturing to produce functional engine parts and structural elements. Metal printing technologies deliver turbine blades and structural brackets that meet strict performance specifications. These functional components reduce aircraft weight and improve thermal resistance. Therefore, defense contractors and commercial airlines both benefit from integrating 3D-printed parts into certified flight hardware.

Major Challenges

High implementation costs create a significant barrier for many aerospace companies considering additive manufacturing adoption. Specialized 3D printing equipment and aerospace-grade materials require substantial upfront capital investment. Smaller firms and emerging market operators often cannot absorb these costs. Additionally, ongoing certification testing adds further financial and timeline burdens on top of initial equipment expenditure.

Strict regulatory requirements slow the integration of 3D-printed components into certified aerospace platforms. Aviation authorities require extensive testing and documentation before approving new manufacturing methods for flight-critical parts. This certification process is both time-consuming and costly. Moreover, a global shortage of technically skilled workers limits the pace at which aerospace firms can scale additive manufacturing operations.

Business Opportunities

Development of new high-performance printable materials opens major growth opportunities across the aerospace additive manufacturing sector. Materials that withstand extreme temperatures and pressure expand the range of engine and structural applications. Companies investing in advanced alloys, high-temperature polymers, and composite blends position themselves to capture premium contract opportunities. Consequently, material innovation drives both revenue growth and competitive differentiation.

Emerging aerospace markets in Asia Pacific, the Middle East, and Latin America present significant expansion opportunities for 3D printing technology providers. Governments in these regions are investing in domestic aerospace capabilities and fleet modernization programs. Additive manufacturing offers cost-effective solutions that align with these nations’ goals. Therefore, early-mover technology providers gain strong positioning in markets that traditional aerospace suppliers have not fully penetrated.

Regional Analysis

North America leads the global aerospace additive manufacturing market, holding a 41% share and generating USD 1.12 billion in revenue in 2023. The region benefits from a dense concentration of major aircraft manufacturers, defense contractors, and research institutions. These organizations invest heavily in next-generation production technologies, maintaining North America’s lead through continuous innovation and R&D spending.

Asia Pacific is the fastest-growing region in this market, driven by expanding aerospace programs in China, India, Japan, and South Korea. According to market.us, China’s government alone committed USD 100 million to aerospace additive manufacturing research in 2023. This funding accelerates domestic production capability. Moreover, Europe sustains strong growth through government-backed R&D programs and deep aerospace manufacturing expertise across Germany, France, and the United Kingdom.

Trusted by industry leaders worldwide. Access the full Aerospace 3D Printing Market report today. Request Your Free Sample

Recent Developments

- In June 2023, Stratasys launched a new 3D printer purpose-built for aerospace production, delivering improved part precision and faster output speeds to meet the demanding requirements of aircraft component manufacturing programs.

- In May 2023, 3D Systems acquired a smaller additive manufacturing firm, expanding its material portfolio for aerospace applications and strengthening its ability to produce more durable, flight-ready components.

- In April 2023, Norsk Titanium secured USD 30 million in new funding to expand production of aerospace-grade titanium parts, with plans to double output capacity and meet growing demand from commercial and defense customers.

Conclusion

The global aerospace 3D printing market is on a strong and sustained growth trajectory through 2033. Demand for lightweight components, faster development cycles, and cost-efficient small-batch production continues to accelerate adoption. Hardware, SLM technology, metal materials, and aircraft platforms will remain the dominant segments driving overall market revenue.

North America leads today, but Asia Pacific is closing the gap rapidly through aggressive government investment and expanding domestic aerospace capability. Material innovation and regulatory progress will determine which companies capture the largest share of emerging opportunities. Moreover, military applications and spacecraft programs offer high-value growth channels beyond commercial aviation.

Stakeholders who invest early in certified additive manufacturing processes, workforce development, and advanced material research will gain lasting competitive advantages. The aerospace 3D printing sector rewards companies that combine technical expertise with scalable production capability. Therefore, strategic investment now positions manufacturers and technology providers for leadership in the next decade of aerospace production.