AI In Procurement Market Size

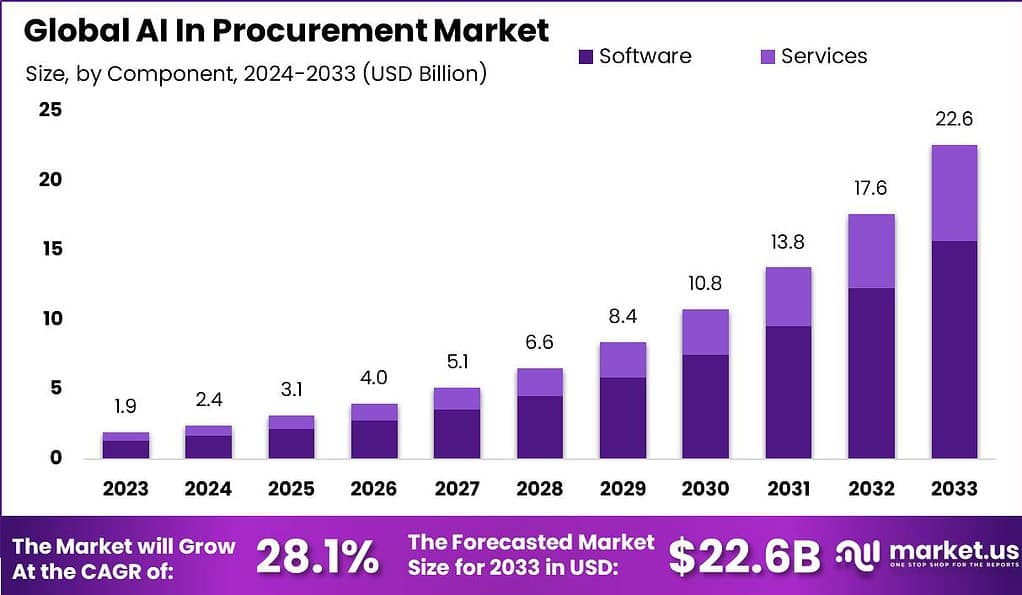

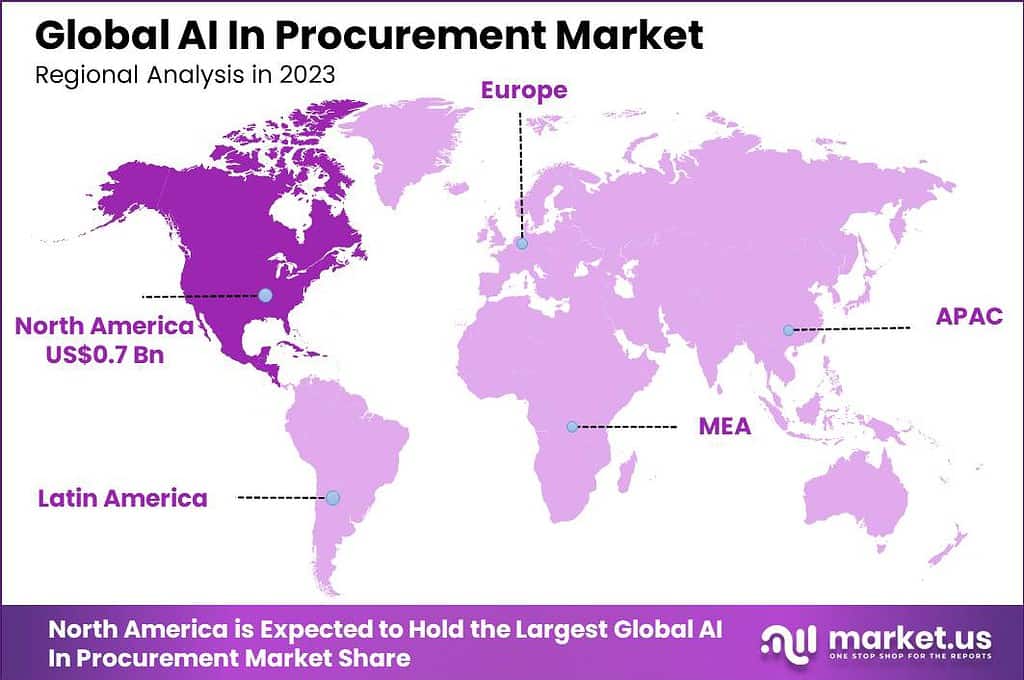

The AI in Procurement market is projected to increase from USD 3.1 billion in 2025 to approximately USD 22.6 billion by 2033, reflecting a compound annual growth rate of 28.1% during the forecast period. In 2023, North America held a leading position with over 38% market share, generating close to USD 0.7 billion in revenue.

AI adoption has become widespread across business functions, including procurement, customer management, and finance operations. According to the provided data, 98% of companies have already incorporated AI into their workflows. This high level of adoption shows that AI is being used to streamline processes, improve decision-making, and increase operational efficiency across multiple departments.

In procurement, AI is increasingly being recognized as a high-impact technology. Research cited in the text shows that 57% of procurement professionals believe AI will significantly affect the industry by 2025, while 35% of procurement organizations are already using AI tools in some capacity. These organizations are seeing measurable benefits, including lower costs and better efficiency, with AI-powered solutions reducing purchasing expenses by up to 8%.

The value of AI in procurement goes beyond direct cost control. AI-driven spend analysis can identify potential savings of up to 20%, while automation can manage as much as 95% of routine procurement tasks. This allows procurement teams to reduce time spent on repetitive manual work and focus more on strategic priorities that support long-term business growth.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

Key Takeaways

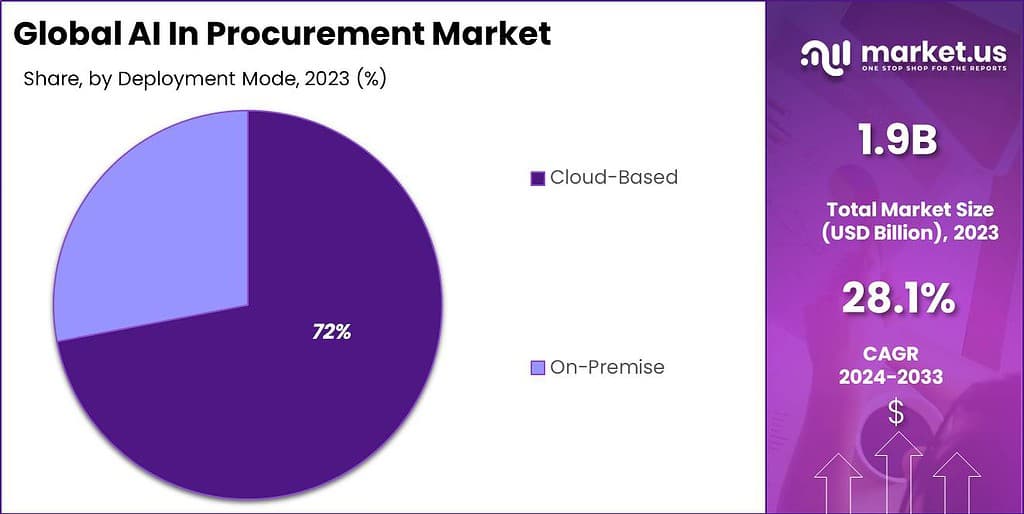

- The global AI in procurement market is projected to reach USD 22.6 billion by 2033, growing from USD 1.9 billion in 2023 at a CAGR of 28.1%.

- North America led the market in 2023 with a share of over 38%, generating nearly USD 0.7 billion in revenue.

- The software segment dominated with 69.5%, reflecting strong demand for AI-driven procurement tools and platforms.

- Cloud deployment accounted for 72% of the market in 2023, supported by scalability, flexibility, and ease of implementation.

- Machine learning led the technology segment with a share of more than 43.4%, driven by its role in improving procurement decisions and process efficiency.

- Retail and e-commerce held over 23.1% of the market, making it the leading industry application segment in 2023.

AI in Procurement Statistics

- Weekly use of generative AI in purchasing and procurement jumped from 50% of executives in 2023 to 94% in 2024, a 44‑point increase in a single year.

- About 49% of procurement teams piloted generative AI in 2024, yet only 4% managed to scale it across the function, showing a wide gap between experimentation and full rollout.

- Roughly 90% of procurement leaders say they have either already adopted or are planning to adopt AI agents to optimize operations in the near term.

- In recent surveys, around 72% of procurement leaders list generative AI integration as a strategic priority, and about 34% are looking at it specifically for data driven analysis of complex spend and risk.

- AI tools in procurement can cut time spent on routine data queries by up to 80%, while adoption among mid sized firms has risen by about 25% over the last two years as cloud tools lower entry barriers.

- Case studies show AI enabled procurement can deliver around 10–20% cost reductions by improving supplier selection, consolidating spend, and optimizing pricing.

- In some data driven implementations, AI helped reduce total procurement costs by 25% in six months, including a 65% drop in purchase order transaction costs and a 22% cut in inventory carrying costs.

- Broader analyses suggest agentic and automation heavy AI in procurement can unlock about 25–40% efficiency improvement potential in end to end processes.

Regional Analysis: North America

In 2023, North America led the AI in procurement market, securing over 38% of the global share and generating approximately USD 0.7 billion in revenue, supported by rapid adoption of advanced technologies. The region has a strong digital infrastructure and early adoption of artificial intelligence across enterprise functions. Organizations are increasingly integrating AI into procurement processes to improve efficiency and reduce operational costs. This has positioned North America as a leading contributor to market growth.

The region’s dominance is further driven by continuous innovation and high investment in AI-driven enterprise solutions. Companies are focusing on automating procurement workflows and enhancing supplier management capabilities. The presence of large enterprises and technology providers further strengthens market expansion. These factors collectively contribute to sustained leadership in the region.

By Component: Software

In 2023, the software segment dominated the AI in procurement market, holding a significant 69.5% share, reflecting strong demand for AI-powered procurement platforms. These solutions enable automation of sourcing, contract management, and supplier evaluation processes. Organizations are adopting software tools to enhance decision-making and improve procurement efficiency. As digital transformation accelerates, software solutions remain central to AI adoption.

The segment’s growth is also supported by advancements in data analytics and automation technologies. AI-driven software helps organizations analyze large datasets and identify cost-saving opportunities. Integration with enterprise systems further enhances workflow efficiency. This has reinforced the dominance of software in the market.

By Deployment: Cloud-based

In 2023, the cloud-based segment held a strong 72% share, driven by increasing preference for scalable and flexible deployment models. Cloud solutions allow organizations to access procurement platforms remotely and manage operations in real time. This improves collaboration and supports efficient data management across multiple locations. As a result, cloud deployment has become the preferred choice for modern enterprises.

The segment’s expansion is further influenced by lower infrastructure costs and faster implementation. Businesses benefit from continuous updates, improved accessibility, and reduced maintenance requirements. Cloud platforms also enable seamless integration with other enterprise applications. This has strengthened their position in the AI in procurement market.

By Technology: Machine Learning

In 2023, machine learning emerged as the leading technology, capturing more than 43.4% of the market share, driven by its ability to enhance decision-making processes. Machine learning algorithms analyze historical procurement data to identify patterns and predict future trends. This helps organizations optimize sourcing strategies and improve supplier performance. As data volumes increase, the importance of machine learning continues to grow.

The segment’s leadership is also supported by its role in automation and predictive analytics. Organizations are leveraging machine learning to reduce manual intervention and improve accuracy in procurement activities. These capabilities enable faster and more informed decisions. This has positioned machine learning as a key technology in the market.

By End-Use Industry: Retail and E-commerce

In 2023, the retail and e-commerce segment accounted for over 23.1% of the market share, reflecting strong adoption of AI in procurement operations. These industries rely on efficient sourcing and supplier management to handle large product volumes and dynamic demand. AI tools help optimize inventory, reduce costs, and improve supply chain efficiency. This has driven widespread adoption in the sector.

The segment’s growth is further supported by increasing competition and the need for operational efficiency. Retailers and e-commerce companies are using AI to enhance procurement strategies and improve responsiveness to market changes. Data-driven insights enable better decision-making and cost optimization. This has reinforced the position of retail and e-commerce as a leading end-use industry in the market.

Key Players Analysis

The AI in Procurement Market is led by major enterprise technology providers offering integrated procurement and analytics platforms. IBM Corporation, SAP SE, Microsoft Corporation, and Oracle Corporation deliver AI-driven solutions for supplier management and spend analysis. These companies focus on automation and data intelligence. Their platforms improve procurement efficiency. This supports better decision-making and cost optimization across organizations.

Procurement-focused software providers play a key role in enhancing sourcing and supplier collaboration. Coupa Software Inc., GEP, and Basware Corporation offer AI-powered procurement solutions. Ivalua Inc. and Zycus Inc. focus on contract management and supplier analytics. These companies enable digital procurement transformation. Their tools enhance visibility and compliance. This improves overall procurement performance.

Emerging and niche players contribute to innovation in procurement automation and workflow optimization. Xeeva, Inc., Tradeshift Holdings, Inc., and Proactis Holdings Limited provide specialized solutions for sourcing and invoicing. These companies focus on AI-driven insights and process automation. Their offerings support scalable procurement operations. Other key players continue to expand capabilities. This competitive landscape supports steady growth in AI-enabled procurement solutions.

Top Key Players in the Market

- IBM Corporation

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Coupa Software Inc.

- GEP

- Basware Corporation

- Xeeva, Inc.

- Zycus Inc.

- Ivalua Inc.

- Tradeshift Holdings, Inc.

- Proactis Holdings Limited

- Other Key Players

Recent Developments

- January, 2026 – SAP Ariba enhanced its AI sourcing optimizer with generative capabilities for RFx automation. Procurement teams generate compliant supplier questionnaires 80% faster. Global enterprises managed EUR 500 billion spend through intelligent workflows.

- February, 2026 – IBM Watson Procurement added cognitive spend clustering for tail spend. AI categorized 95% of maverick purchases automatically. Fortune 500 firms consolidated vendors 30% while cutting costs 12%.

Report Scope

| Report Features | Description |

| Market Value (2023) | USD 1.9 Bn |

| Forecast Revenue (2033) | USD 22.6 Bn |

| CAGR (2024-2033) | 28.10% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), By Technology (Machine Learning (ML), Natural Language Processing (NLP), Computer Vision, Other Technologies), By Industry Vertical (Retail and E-commerce, Manufacturing, Healthcare, Transportation and Logistics, Government and Public Sector, Other Industry Verticals) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | IBM Corporation, SAP SE, Microsoft Corporation, Oracle Corporation, Coupa Software Inc., GEP, Basware Corporation, Xeeva, Inc., Zycus Inc., Ivalua Inc., Tradeshift Holdings, Inc., Proactis Holdings Limited, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |