Market Overview

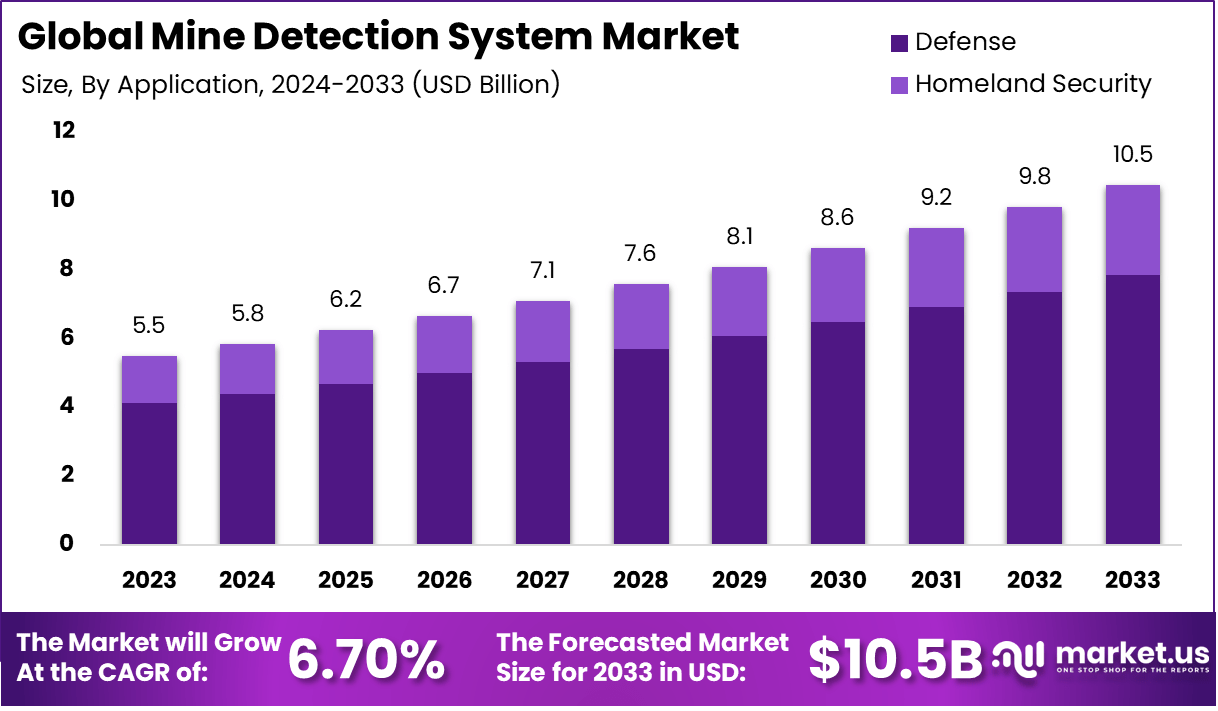

The global Mine Detection System market is projected to grow from USD 5.48 billion in 2023 to USD 10.5 billion by 2033, at a CAGR of 6.70% during the forecast period from 2024 to 2033. This steady expansion reflects rising global demand for landmine clearance technologies across both military and humanitarian sectors.

Mine detection systems identify and locate landmines or unexploded ordnance (UXOs) buried underground or submerged in water. Defense forces, humanitarian organizations, and governments use these systems to protect personnel, enable safe reconstruction, and clear land for agricultural or civilian use in post-conflict regions.+

Get further insight into the global trends shaping the future of the mine detection industry. Request Sample

Several sectors actively drive adoption of mine detection technologies. The defense industry relies on these systems for troop safety and route clearance. Humanitarian organizations use them to restore farmland and infrastructure. Construction and infrastructure sectors also deploy mine detection solutions before beginning projects in conflict-affected areas.

Technology advancements are rapidly improving detection capabilities. AI-powered systems now analyze data in real time, reducing false positives. Robotics and autonomous unmanned vehicles lower human risk during clearance operations. Improved sensor miniaturization also enables portable, handheld devices suited for remote or densely vegetated terrain.

Regulatory support from international bodies is accelerating market growth. The United Nations and the International Committee of the Red Cross fund mine-clearance initiatives globally. Government defense budgets in the United States, Europe, and Asia-Pacific are also increasing allocations for advanced demining equipment and modernization programs.

Related market data highlights the urgency driving this sector. The United Nations Mine Action Service (UNMAS) reports that over 60 countries still suffer from active landmine contamination. Global annual casualties from landmines and UXOs reach approximately 4,000, underscoring critical demand for faster and more precise detection solutions worldwide.

Key Takeaways

- The global Mine Detection System market grows from USD 5.48 billion in 2023 to USD 10.5 billion by 2033, at a CAGR of 6.70%.

- Vehicle-mounted systems lead the deployment segment with a 40% market share in 2023, valued for their speed and terrain adaptability.

- The Defense application segment dominates with 75% of total market share in 2023, reflecting ongoing military reliance on mine clearance operations.

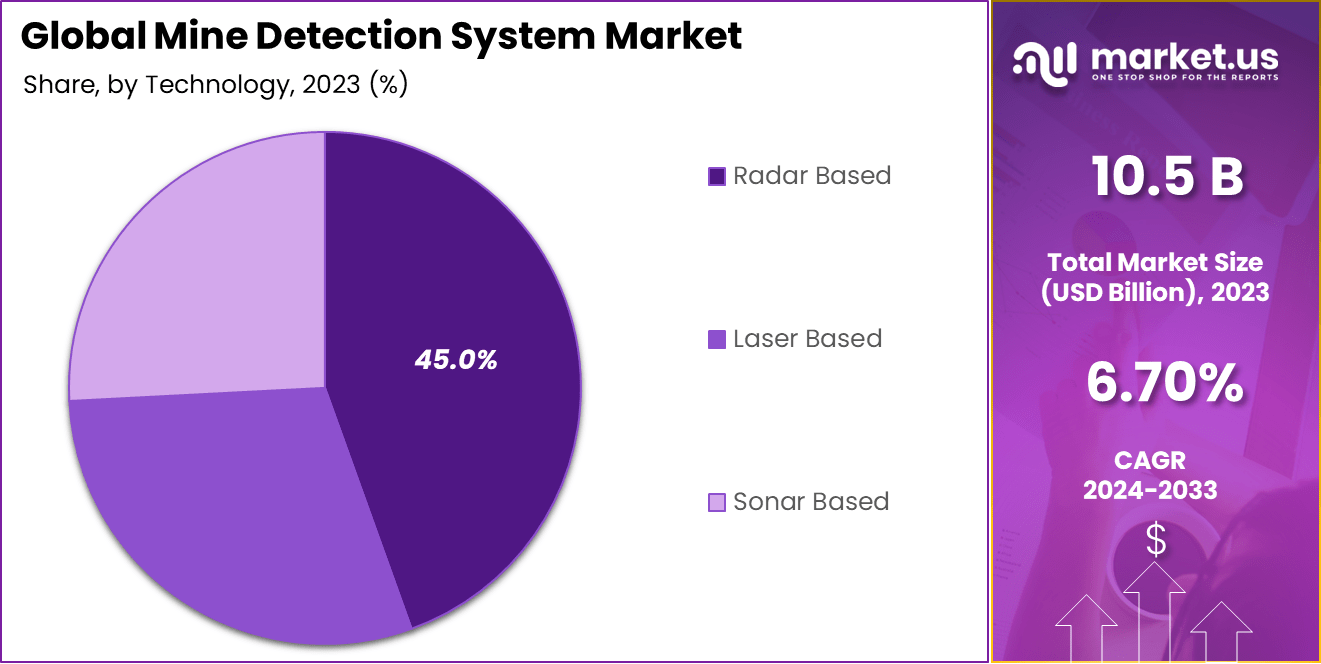

- Radar-based technology holds the largest technology segment share at 45% in 2023, preferred for deep detection across varied soil conditions.

- OEMs capture 60% of the upgrades segment, driven by continuous innovation and strong partnerships with defense organizations.

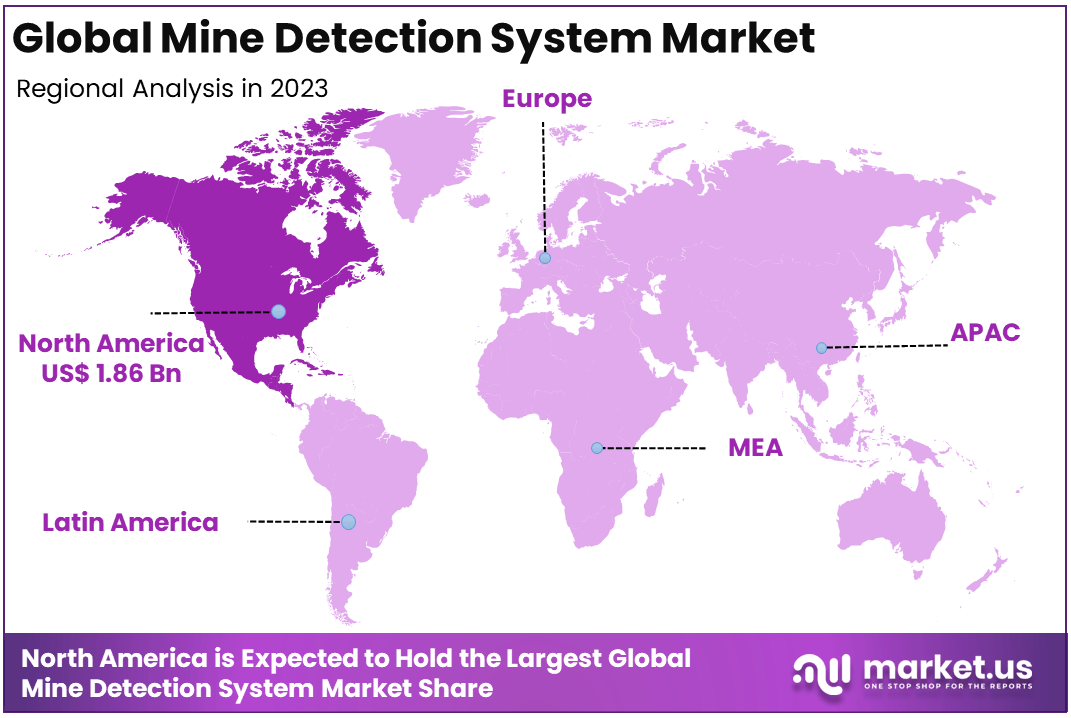

- North America leads all regions with 34% market share and USD 1.86 billion in revenue in 2023.

- Over 60 countries remain affected by landmines, sustaining long-term global demand for mine detection solutions.

Market Segmentation Overview

Vehicle-mounted mine detection systems lead the deployment segment, capturing more than 40% of market share in 2023. These systems cover large areas quickly across diverse terrains, from deserts to rugged conflict zones. Their compatibility with ground-penetrating radar (GPR) and electromagnetic induction sensors makes them essential for both military and humanitarian clearance operations.

The Defense application segment commands more than 75% of total market share in 2023. Military forces worldwide depend on mine detection technologies to secure routes, protect personnel, and enable safe troop movement. The Homeland Security segment, while smaller, is growing as governments prioritize civilian protection in previously conflict-affected territories.

Radar-based mine detection technology holds 45% of the technology segment in 2023. Its ability to detect both metallic and non-metallic mines at varying depths makes it highly reliable. Laser-based systems account for approximately 15%, while sonar-based systems represent around 10%, serving specialized maritime and underwater demining applications.

OEMs dominate the upgrades segment with a 60% share in 2023. They design and manufacture systems incorporating radar, laser, and sonar technologies that meet evolving defense requirements. MROs support the remaining share by maintaining operational systems, ensuring performance standards across extended product lifecycles in active deployment environments.

Drivers

Growing military demand across conflict-prone regions powerfully drives mine detection system adoption. Nations in the Middle East, Africa, and Southeast Asia face persistent landmine threats that endanger soldiers and civilians alike. Defense agencies worldwide are investing in radar-based, sonar-based, and AI-enhanced detection systems to improve clearance speed, accuracy, and personnel safety during operations.

Technological innovation in sensors, AI, and robotics significantly accelerates market expansion. AI algorithms now identify potential mine locations in real time, reducing false positives and improving operator confidence. Unmanned ground vehicles and robotic platforms further reduce human exposure to hazards, enabling faster and more cost-effective demining across difficult environments globally.

Use Cases

Military forces deploy vehicle-mounted and robotic mine detection systems to secure routes and protect troops in active conflict zones. These systems use ground-penetrating radar and electromagnetic sensors to locate IEDs and buried landmines before troop movement. Faster route clearance directly reduces soldier casualties and improves mission success rates in high-risk operational theaters.

Moreover, humanitarian organizations use mine detection systems to restore farmland and enable reconstruction in post-conflict nations. Countries across Africa, Southeast Asia, and Eastern Europe rely on demining operations to reclaim agricultural land and rebuild civilian infrastructure. Cleared land enables resettlement, reduces poverty, and supports long-term economic recovery in communities devastated by conflict.

Major Challenges

The high cost of advanced mine detection systems presents a significant barrier to adoption, particularly for low- and middle-income countries. Acquiring, operating, and maintaining radar-based or sonar-based systems demands substantial budgets. Training skilled operators adds further financial burden. Governments with limited defense funding often settle for less precise, lower-cost alternatives that compromise mission safety and effectiveness.

Additionally, operating mine detection systems in harsh environments creates serious performance limitations. Dense vegetation, mountainous terrain, swamps, and extreme weather conditions reduce detection accuracy and equipment reliability. Rain, high humidity, and temperature extremes can trigger false positives and disrupt sensor functionality. These environmental constraints slow clearance operations and increase operational risk in the world’s most landmine-affected regions.

Business Opportunities

AI and machine learning integration creates a major growth opportunity for mine detection system manufacturers. AI-driven systems analyze real-time sensor data to distinguish threats from harmless objects with greater precision. Companies that develop autonomous, self-learning detection platforms can capture growing defense and humanitarian contracts, especially in regions where dense terrain complicates traditional detection approaches.

Consequently, rising naval security concerns are fueling demand for underwater mine detection solutions. Naval forces and maritime organizations worldwide seek advanced sonar-based systems to clear waterways and protect shipping lanes. Companies that develop compact, high-performance underwater detection platforms will benefit as coastal nations increase maritime defense spending and international trade security requirements tighten.

Regional Analysis

North America dominates the global mine detection system market with a 34% share and USD 1.86 billion in revenue in 2023. The United States drives this leadership through heavy defense investment and active deployment in post-conflict zones. Companies like Raytheon Technologies and Lockheed Martin continuously develop cutting-edge radar and GPR solutions, maintaining North America’s technological advantage in global demining operations.

Asia-Pacific is emerging as a high-growth region, with India and China increasing investments in advanced detection technologies. Europe contributes approximately USD 1.2 billion, driven by active demining programs in Ukraine and Bosnia and Herzegovina. The Middle East and Africa also present strong demand, as ongoing and post-conflict environments sustain urgent requirements for both military and humanitarian mine clearance solutions.

Recent Developments

- June 2023 — BAE Systems launched an upgraded version of its Husky vehicle-mounted mine detection system, incorporating advanced radar and sensor technology to improve detection accuracy and operational efficiency in conflict environments.

- August 2023 — Israel Aerospace Industries (IAI) unveiled its next-generation unmanned ground vehicle (UGV) for mine detection, designed to autonomously navigate and identify landmines using a combination of radar and ground-penetrating radar (GPR) technologies.

Conclusion

The global mine detection system market is on a strong and sustained growth trajectory. Rising geopolitical tensions, persistent post-conflict landmine threats, and increasing defense budgets are compelling governments and military organizations worldwide to adopt advanced demining technologies. Continuous innovation in radar, AI, and autonomous systems will remain central to this market’s expansion through 2033.

Vehicle-mounted systems and defense applications dominate current market activity, reflecting where the most critical operational needs exist. Radar-based technology leads the technology segment due to its versatility and deep detection capability. North America retains market leadership, while Asia-Pacific and Europe are rapidly expanding their investments in both military and humanitarian mine clearance programs.

Companies that invest in AI-driven autonomous systems, underwater detection capabilities, and partnerships with defense agencies will be best positioned to capture emerging opportunities. Businesses that ad dress cost barriers through modular and scalable product designs will also gain access to underserved markets in conflict-affected developing regions. The global mine detection system market is forecast to reach USD 10.5 billion by 2033.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at [email protected]