Agentic AI in Energy Market Size

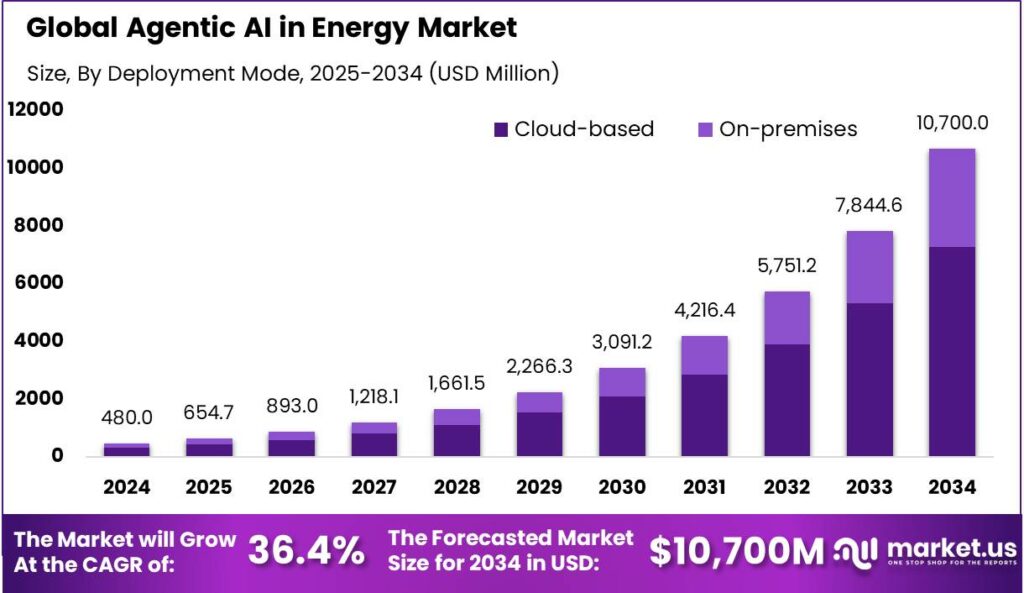

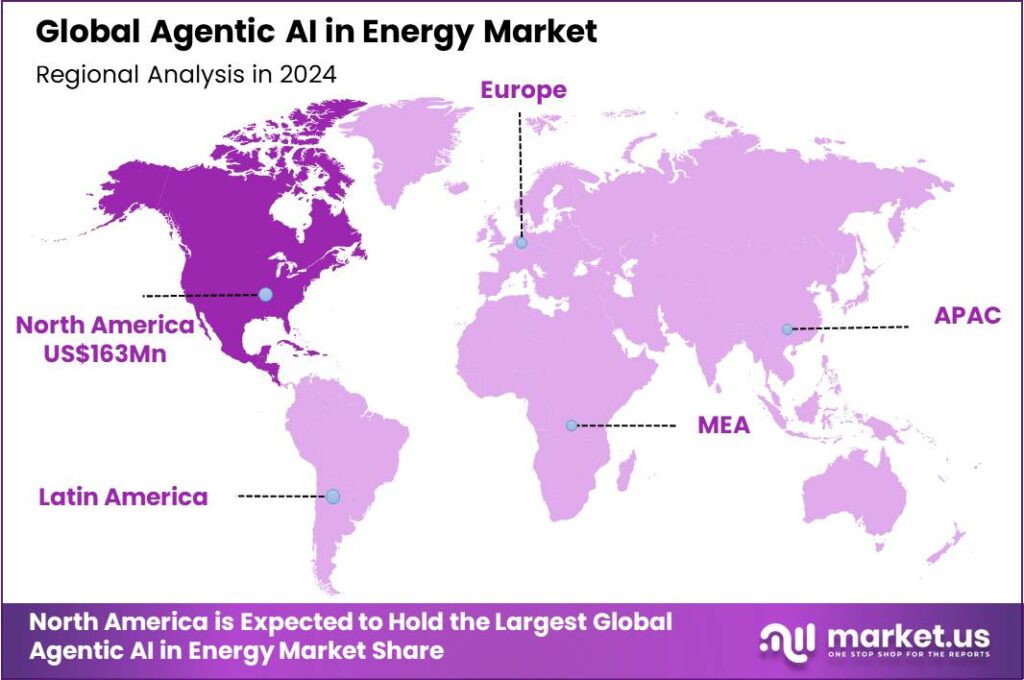

According to Market.us, the Global Agentic AI in Energy Market is projected to reach USD 10,700 million by 2034, up from USD 480 million in 2024, registering a robust CAGR of 36.40% over the forecast period. The rising integration of intelligent, autonomous AI systems in the energy sector is unlocking new efficiencies across generation, storage, and distribution. In 2024, North America led the market with a 34% share and approximately USD 163 million in revenue, signaling strong early adoption in advanced economies.

Get further insight into the global trends that are affecting the future of the Energy industry. Request Sample @ https://market.us/report/agentic-ai-in-energy-market/request-sample/

Top driving factors include increasing demand for energy efficiency optimization, the push for grid modernization, and the rising need for predictive energy management systems. Governments and energy corporations are investing heavily in AI-enabled automation to manage demand fluctuations, enhance forecasting, and support sustainable energy transitions. Additionally, the adoption of AI-driven digital twins and autonomous analytics across smart grids has become a cornerstone for operational improvement.

Demand analysis reveals that both utilities and private energy enterprises are leveraging AI to improve real-time decision-making and reduce carbon footprints. The market’s growth is particularly fueled by the rise in renewable energy integration, where Agentic AI models enhance load balancing and power dispatching. Meanwhile, the commercial and industrial sectors are adopting these solutions to optimize facility performance while reducing costs.

Top Market Takeaway

- The Platform/Software Solutions segment held the highest share in 2024, accounting for over 66% of the total market.

- The Cloud-Based segment led the deployment category, with more than 68% share in 2024.

- The Smart Grid Management application segment dominated, capturing over 22% of the overall application market.

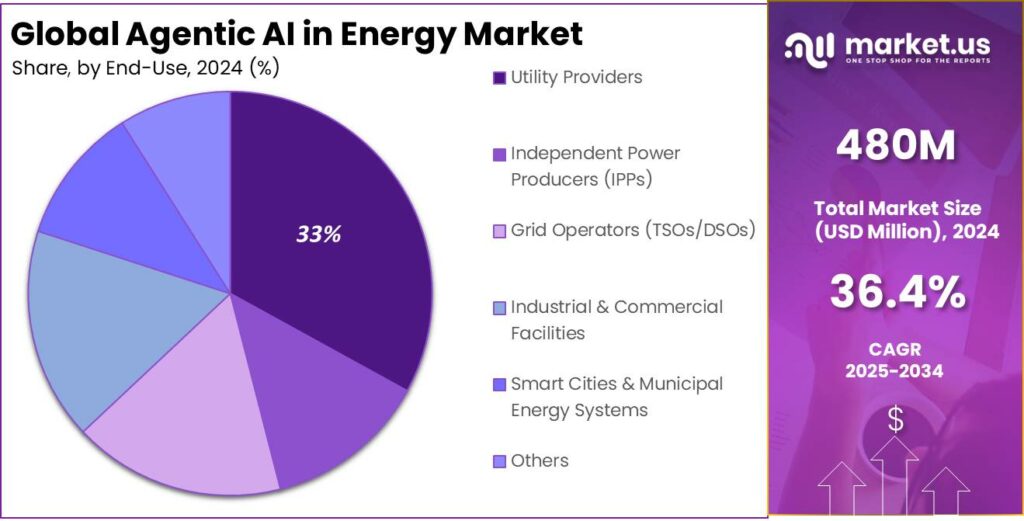

- The Utility Providers segment was the largest end-user group with over 33% share in 2024.

- North America remained the leading regional market with over 34% share and nearly USD 163 million in revenue in 2024.

Report Scope

| Report Features | Description |

| Market Value (2024) | USD 480 Mn |

| Forecast Revenue (2034) | USD 10,700 Mn |

| CAGR (2025-2034) | 36.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Platform/Software (Solutions (Grid Monitoring & Optimization Agents, Energy Trading & Market Forecasting Agents, Predictive Maintenance Agents, Demand Forecasting & Load Balancing Agents, Emissions Monitoring & Compliance Agents), Services (System Integration, Support & Managed Services, AI Model Training & Fine-Tuning)), By Deployment Mode (Cloud-Based, On-Premises), By Application (Smart Grid Management, Distributed Energy Resource (DER) Optimization, and Others), By End-Use (Utility Providers, Independent Power Producers (IPPs), Grid Operators (TSOs/DSOs), Industrial & Commercial Facilities, Smart Cities & Municipal Energy Systems, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Microsoft, Google, IBM, Schneider Electric, Siemens, Amazon Web Services (AWS), NVIDIA, Salesforce, Baidu, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Component Segment

The Platform/Software Solutions segment dominated the global Agentic AI in Energy Market, accounting for over 66% share in 2024. These AI-driven platforms provide autonomous, adaptive solutions that allow energy companies to manage their operations more effectively. They integrate seamlessly with existing systems to optimize energy consumption, reduce operational costs, and improve forecasting accuracy. This segment’s strong growth reflects energy providers’ increasing demand for intelligent control software that supports real-time analytics and decision-making.

Beyond efficiency, these platforms are enabling decentralized energy management through digital twins, automated monitoring, and multi-agent coordination systems. As energy infrastructures modernize globally, software-based AI ecosystems have become the backbone of next-generation power management. This trend is expected to continue as energy companies seek to gain more flexible, cloud-integrated solutions that can adjust dynamically to grid fluctuations and user demand.

Deployment Model

The Cloud-Based deployment segment captured a commanding 68% market share in 2024, reinforcing the shift toward scalable, real-time digital energy management. Cloud computing enables remote monitoring, distributed analytics, and centralized system oversight, reducing infrastructure costs while improving data transparency. Energy utilities increasingly rely on cloud-hosted AI to manage fluctuating supply and demand, guided by continuous data from IoT sensors and intelligent control systems. This architecture supports rapid deployment and integration with renewable energy sources.

Additionally, hybrid and multi-cloud environments are gaining traction to maintain data security, flexibility, and interoperability. As Agentic AI models evolve, the need for high-performance computing and continuous updates through cloud interfaces increases. Industry leaders are thus investing in cloud-native design frameworks to enable faster model training and distributed energy intelligence that scales seamlessly across regions and energy sources.

Application Segment

The Smart Grid Management application segment dominated the Agentic AI in Energy Market with over 22% share in 2024. The integration of AI technologies helps manage fluctuating demand patterns through real-time insights, predictive analytics, and automated load adjustments. Agentic AI systems analyze grid conditions continuously, identifying inefficiencies and potential points of failure before disruptions occur. The ability to integrate renewable energy sources smoothly also makes this segment strategically crucial to developing future energy ecosystems.

Smart grid management with Agentic AI is accelerating digital transformation across utilities and public infrastructure. The deployment of intelligent agents across network nodes allows decentralized decision-making and improved power distribution efficiency. Moreover, AI-powered energy optimization drives lower emissions and reduces waste, aligning with global sustainability goals. The evolution of smart grids is expected to serve as a cornerstone for autonomous power networks in the next decade.

End-User Segment

Utility Providers accounted for over 33% share of the global Agentic AI in Energy Market in 2024, maintaining their dominance as key adopters of intelligent automation. Major utility companies are integrating Agentic AI platforms for fault detection, energy load forecasting, and grid optimization. These systems improve operational uptime and resilience by predicting component failures and automating maintenance workflows. The adoption also supports improved regulatory compliance and enhanced customer service through better power distribution analytics.

As energy networks expand to accommodate renewables, utilities are leveraging AI to balance power flow, integrate distributed energy resources, and forecast peak demand efficiently. AI-driven decision-making is helping public and private utilities transition from reactive to predictive operations. This transition not only enhances grid efficiency but also supports broader decarbonization initiatives, making utility providers the leading beneficiaries of AI-enabled modernization in the energy landscape.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Regional Outlook

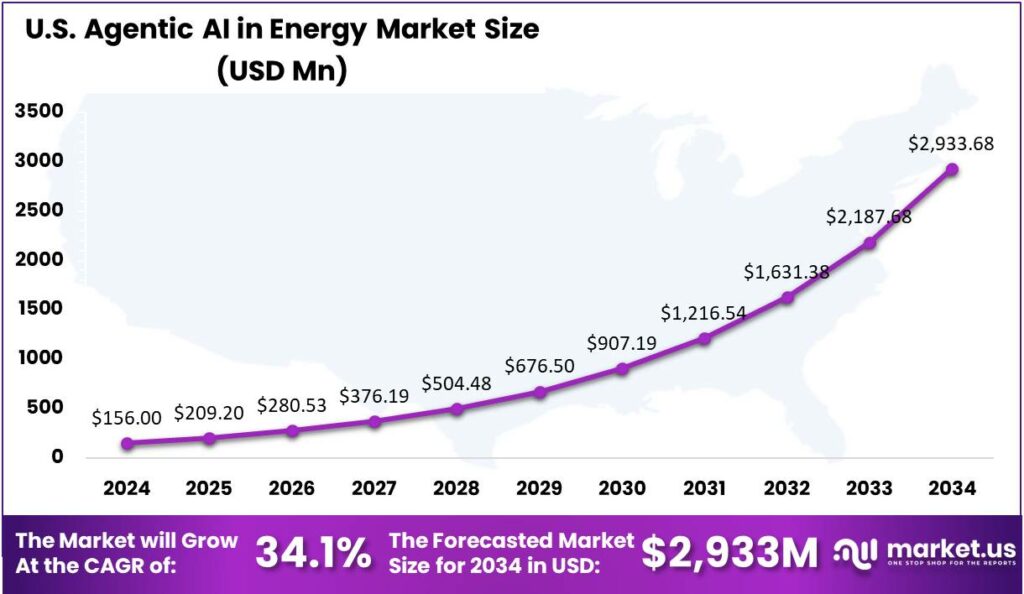

North America led the Agentic AI in Energy Market with over 34% share in 2024, translating to around USD 163 million in revenue. The United States accounted for the majority of this share, driven by rapid adoption of AI technologies and grid modernization programs. Strong investments from both public and private organizations, alongside initiatives for sustainable energy transition, are fueling regional growth. The technological maturity of this market allows faster adoption of agent-based AI for predictive and distributed energy systems.

Government-backed projects supporting AI-driven clean energy deployment further bolster the region’s competitive edge. North American energy providers are early adopters of AI for efficiency improvements, emission reduction, and digital infrastructure upgrades. The region’s expertise in data science and robust partnerships with AI tech firms ensure continuous innovation. With a forecasted 34.1% CAGR, the U.S. is expected to maintain its leading role in global AI-for-energy solutions throughout the next decade.

Competitive Analysis

Microsoft, Google, and IBM are leading the Agentic AI in Energy market through advanced AI infrastructure, cloud solutions, and analytics platforms tailored for energy management. Each player leverages large-scale data ecosystems to provide predictive insights and operational automation across the value chain. Siemens and Schneider Electric focus heavily on integrating AI with industrial automation and smart grid systems, offering AI-driven controllers and monitoring platforms that boost energy efficiency at scale.

Their technology-driven solutions support real-time operational intelligence for grid operators and manufacturers. Emerging entrants such as NVIDIA, AWS, and Salesforce are investing in AI model development, cloud-native energy AI tools, and ecosystem partnerships. Meanwhile, Baidu is expanding its influence in the Asia-Pacific region with localized AI energy management tools designed for large-scale renewable integration.

Top Key Players in the Market

- Microsoft

- IBM

- Schneider Electric

- Siemens

- Amazon Web Services (AWS)

- NVIDIA

- Salesforce

- Baidu

- Others

Market Share

- Microsoft (Market Share: ~11%): Microsoft dominates the Agentic AI in Energy space through Azure AI and cloud-powered grid solutions. Its platforms enable autonomous control, predictive analytics, and sustainable energy optimization at scale. The company’s commitment to carbon-negative operations by 2030 has accelerated its investment in AI-driven sustainability initiatives within the power sector.

- Google (Market Share: ~10%): Google leverages its AI and cloud infrastructure to build energy optimization models that reduce waste and enhance renewable integration. Through Google Cloud’s advanced data services, the company provides scalable analytics tools for utilities, helping minimize carbon output. Its focus on clean energy and algorithmic optimization sustains strong momentum in the market.

- IBM (Market Share: ~8%): IBM’s Watson AI and cognitive computing platforms help utilities forecast energy demand, detect anomalies, and optimize workloads. The company emphasizes integrating AI with IoT for intelligent grid operations. Its decades-long presence in industrial analytics positions IBM as a key enabler of agent-based energy ecosystems.

- Schneider Electric (Market Share: ~7%): Schneider Electric focuses on smart energy management and automation by embedding AI agents into its digital twin and grid controllers. Its EcoStruxure platform exemplifies real-time decision support for industrial and utility clients. The company’s AI integration allows greater visibility into energy flows across distributed infrastructures.

- Siemens (Market Share: ~9%): Siemens leads in industrial digitization and power systems automation. Its AI-based grid management solutions combine real-time analytics and predictive diagnostics to maintain continuous power reliability. Siemens’ investment in digital twin technologies strengthens its competitive role in next-gen grid transformation initiatives.

- Amazon Web Services (AWS) (Market Share: ~8%): AWS provides cloud-based energy intelligence through scalable AI, machine learning, and edge processing solutions. Utility firms use AWS’s infrastructure to deploy autonomous energy agents for grid monitoring and optimization. Its robust ecosystem and collaborations with global utilities reinforce its leadership in cloud-native energy AI solutions.

- NVIDIA (Market Share: ~6%): NVIDIA contributes strongly through AI computing hardware and simulation environments optimized for energy analytics. Its GPU-based architectures enable rapid AI model training and predictive simulation of power networks. Through partnerships with key energy firms, NVIDIA supports advanced AI agent modeling and grid demand forecasting.

- Salesforce (Market Share: ~5%): Salesforce integrates AI tools into its sustainability and asset management solutions for energy providers. Its AI-powered CRM and workflow capabilities support analytics-driven decision-making for energy operations. By embedding intelligent process automation, Salesforce contributes to operational transparency and customer engagement in the energy sector.

- Baidu (Market Share: ~4%): Baidu’s expansion in the Asia-Pacific region focuses on developing localized Agentic AI solutions for renewable integration and grid management. Leveraging its extensive expertise in AI infrastructure, the company delivers scalable software and digital platforms for power optimization. Its R&D focus on energy efficiency positions it as an emerging competitor globally.

- Others (Market Share: ~32%): The remaining market share is distributed among regional players, startups, and niche AI providers. These companies specialize in grid automation, energy optimization algorithms, and domain-specific analytics platforms. Continuous innovation from smaller entrants is introducing agile, scalable alternatives that accelerate AI adoption beyond major industry incumbents.

Recent News and Developments

- December 2025: Microsoft launched a new AI-powered energy optimization suite incorporating multi-agent systems for grid balancing and sustainability reporting.

- October 2025: Siemens announced a partnership with AWS to integrate generative AI capabilities into its smart grid management platform.

- February 2026: IBM introduced an Agentic AI analytics engine designed for real-time energy demand forecasting in high-volatility markets.

- January 2026: Schneider Electric announced collaboration with NVIDIA to co-develop digital twin solutions for energy infrastructure monitoring.

Conclusion

The Global Agentic AI in Energy Market is on a transformative growth path, with the potential to redefine the energy landscape through automation, intelligence, and sustainability. Fueled by rapid platform and cloud adoption, the market’s future lies in scaling self-governing AI systems capable of real-time optimization and strategic energy distribution. As governments and corporations accelerate toward decarbonization goals, Agentic AI will become the cornerstone of modern, resilient, and adaptive energy systems worldwide.