AI Agents Market Size

The Global AI Agents Market is projected to reach approximately USD 139.12 billion by 2033, rising significantly from USD 3.66 billion in 2023. This strong expansion reflects a compound annual growth rate of 43.88% over the forecast period from 2024 to 2033. In 2023, North America maintained a leading position in the market, accounting for over 37.92% of the total share and generating around USD 1.3 billion in revenue.

Request a sample to learn more about this report @ https://market.us/report/ai-agents-market/request-sample/

Top Market Takeaways

- The global AI agents market is projected to grow from USD 3.66 billion in 2023 to USD 139.12 billion by 2033, registering a CAGR of 43.88%.

- In 2023, North America led the market with a share of over 37.92%, generating approximately USD 1.3 billion in revenue.

- In 2023, the Ready-to-Deploy Agents segment dominated the market, capturing more than 69.19% of the total share.

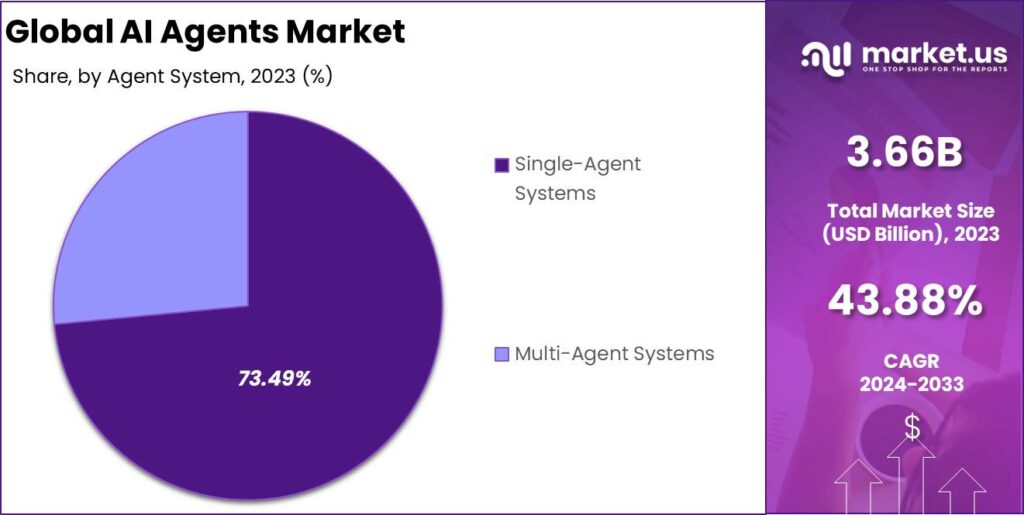

- In 2023, Single Agent Systems held a strong position, accounting for over 73.49% of the market.

- In 2023, Customer Service and Virtual Assistants represented a key application area, securing more than 34.85% share.

- In 2023, the Enterprise segment led adoption, holding over 58.74% of the overall market share.

Market Overview

AI agents are software entities that use artificial intelligence techniques such as machine learning, natural language processing and sometimes computer vision to understand goals, make decisions and execute tasks on behalf of users or systems. They sit on top of enterprise data and tools, interact via text or voice, trigger workflows in CRMs, ERPs or ticketing systems and report back with outcomes, making them ideal for customer support, IT operations, HR, finance and many other functions. In simple terms, they behave like specialized digital colleagues that handle routine and semi‑complex activities, while humans focus on higher‑value work.

A key driver is the rapid adoption of generative AI and large language models, which has made AI agents more natural to talk to and far better at handling open‑ended queries than earlier rule‑based systems. Enterprises now see agents as a practical way to turn these models into operational tools that can automate workflows, reduce repeat contacts and support always‑on service. At the same time, pressure to improve productivity without linearly increasing headcount is pushing organizations to embrace automation that can scale across business units.

Demand is particularly strong in environments with high interaction volumes and standardized processes, such as contact centers, IT helpdesks, banking, e‑commerce and digital‑first services. The strong showing of customer service and virtual assistants as a leading application area reflects this pattern, with these use cases alone accounting for more than 34.85% of AI agent deployments in 2023. Enterprises are also extending agents into back‑office roles like HR case management and finance operations, where they can triage requests, gather information and prepare decisions for human approval.

Contact Sales for Further Assistance in Purchasing this Report

Investment opportunities and Business benefits

The market input data highlights that ready‑to‑deploy agents already captured over 69.19% of the market in 2023, reflecting strong appetite for out‑of‑the‑box solutions that can be configured rather than built from scratch. Single agent systems also held more than 73.49% share in 2023, showing that many organizations still begin with focused, individual agents before exploring more complex multi‑agent setups. Investors can find attractive opportunities in verticalized agents for industries like healthcare, BFSI and retail, as well as in platforms that provide reusable frameworks, orchestration and observability for large fleets of agents.

From a business standpoint, AI agents help compress handling times, cut backlogs and increase first‑contact resolution, which translates directly into better customer experience and lower operating costs. They also improve consistency, because policies and knowledge bases are applied the same way every time, reducing errors and compliance risks. For employees, agents act as smart copilots that surface answers, draft responses and automate routine updates, which can raise job satisfaction and free time for more complex problem‑solving.

Agent Type Insights

The market is segmented into Ready to Deploy Agents and other customized or build from scratch solutions. Ready to Deploy Agents accounted for over 69.19% of the market in 2023, reflecting a strong preference for solutions that can be implemented quickly with limited internal development. This indicates that enterprises are looking for predictable, low friction ways to adopt AI agents without building entire stacks on their own. Vendors offering configurable, out of the box agents with robust integration options are therefore well positioned.

The dominance of Ready to Deploy solutions also shows that many organizations are still at an early or intermediate level of AI maturity. They want to see rapid impact on customer service, operations and support before committing to large, bespoke initiatives. This creates an attractive opening for platform providers and system integrators to layer services, customization and vertical expertise on top of standard agent products. Over time, some of these deployments may evolve into more tailored architectures, but the first step for most buyers is quick, reliable activation.

By Agent Type, 2020-2024 (USD Billion)

| Agent Type | 2020 | 2021 | 2022 | 2023 | 2024 |

| Build-Your-Own Agents | 0.374 | 0.541 | 0.781 | 1.129 | 1.63 |

| Ready-to-Deploy Agents | 0.862 | 1.235 | 1.77 | 2.355 | 3.635 |

Agent System Insights

The market is divided into Single Agent Systems and Multi Agent Systems. Single Agent Systems dominated in 2023, holding more than 73.49% share, which shows that most organizations begin their AI journey with focused, task specific agents. These systems usually handle a clearly defined function such as answering customer queries, supporting IT helpdesks or assisting with internal knowledge search. Their clarity of purpose makes them easier to deploy, monitor and optimize compared to more complex agent networks.

By Agent System, 2020-2024 (USD Billion)

| Agent System | 2020 | 2021 | 2022 | 2023 | 2024 |

| Multi-Agent Systems | 0.325 | 0.468 | 0.674 | 0.971 | 1.399 |

| Single-Agent Systems | 0.912 | 1.308 | 1.876 | 2.693 | 3.865 |

The strong position of Single Agent Systems also reflects risk management and change management considerations inside enterprises. Starting with one well scoped agent allows businesses to test reliability, user acceptance and integration challenges before expanding to broader architectures. As comfort levels grow and internal capabilities improve, companies can gradually move toward orchestrated Multi Agent Systems that handle multi step workflows. In the near term, however, single agents are likely to remain the entry point and mainstay of many deployments.

Application Insights

By application, AI agents are segmented into Customer Service and Virtual Assistants and other use cases such as IT support, sales assistance and back office automation. Customer Service and Virtual Assistants represented over 34.85% of the market in 2023, underlining the central role of AI agents in handling customer queries and improving service quality. These agents typically manage common questions, order status checks, billing issues and simple troubleshooting across chat, email and voice channels. Their impact is visible through reduced wait times, higher self service rates and more consistent responses.

AI agents market Revenue, Application Analysis, 2020-2024 (USD Billion)

| Application | 2020 | 2021 | 2022 | 2023 | 2024 |

| Customer Service and Virtual Assistants | 0.426 | 0.614 | 0.885 | 1.277 | 1.839 |

| Sales and Marketing | 0.292 | 0.424 | 0.614 | 0.891 | 1.287 |

| Human Resources | 0.149 | 0.213 | 0.304 | 0.434 | 0.617 |

| Legal and Compliance | 0.093 | 0.131 | 0.186 | 0.266 | 0.375 |

| Financial Services | 0.171 | 0.246 | 0.353 | 0.504 | 0.728 |

| Other Applications | 0.106 | 0.149 | 0.211 | 0.294 | 0.421 |

Beyond customer facing interactions, the same underlying technologies are increasingly used internally. For example, AI agents can help employees navigate knowledge bases, request HR support or log IT incidents more efficiently. This reuse of core capabilities across external and internal touchpoints makes investments in AI agents more attractive. It also creates a pathway for organizations to extend successful customer service deployments into adjacent functions without rebuilding from the ground up.

End-User Insights

By end user, the market is categorized into Enterprise and other segments such as small and medium sized businesses and individual or consumer oriented deployments. The Enterprise segment led the market with more than 58.74% share in 2023, highlighting that large organizations are the primary adopters of AI agents today. These enterprises typically manage high interaction volumes, complex service portfolios and multi region operations, which makes automation particularly valuable. They also have the budgets, data assets and IT infrastructure required to scale AI initiatives.

AI agents market Revenue, End-User Analysis, 2020-2024 (USD Billion)

| End-User | 2020 | 2021 | 2022 | 2023 | 2024 |

| Enterprise | 0.726 | 1.043 | 1.499 | 2.152 | 3.095 |

| Consumer | 0.296 | 0.427 | 0.618 | 0.894 | 1.293 |

| Industrial | 0.215 | 0.306 | 0.435 | 0.618 | 0.877 |

| Total | 1.237 | 1.776 | 2.551 | 3.664 | 5.265 |

For enterprises, AI agents are not just a cost cutting tool but a way to redesign how work is done. They support strategic goals like improving customer experience, increasing employee productivity and enabling 24/7 operations without linear increases in staffing. As success stories accumulate, AI agents are moving from isolated projects to standard components within digital transformation roadmaps. This momentum in the enterprise segment is likely to influence best practices, standards and expectations for the rest of the market over the coming years.

Regional Highlights: a global perspective

Regionally, North America currently leads the AI agents market, supported by advanced digital infrastructure, high cloud adoption and strong presence of major AI providers, giving it more than 37.92% share in 2023, or around USD 1.3 billion in revenue. The region benefits from early adoption in sectors such as technology, financial services and online retail, which often act as reference cases for the rest of the world. At the same time, Asia Pacific is emerging as a fast‑growing region as businesses accelerate investments in automation and digital customer engagement.

Market Revenue, Regional Analysis, 2020-2024 (USD Billion)

| Region | 2020 | 2021 | 2022 | 2023 | 2024 |

| North America | 0.47 | 0.675 | 0.969 | 1.39 | 2 |

| Europe | 0.308 | 0.442 | 0.635 | 0.909 | 1.309 |

| Asia-Pacific | 0.364 | 0.524 | 0.754 | 1.087 | 1.566 |

| Latin America | 0.057 | 0.081 | 0.116 | 0.166 | 0.234 |

| Middle East & Africa | 0.038 | 0.054 | 0.077 | 0.113 | 0.157 |

Within North America, enterprises are moving quickly from pilots to scaled deployments, especially in customer service, IT operations and sales support use cases. A strong ecosystem of cloud providers, software vendors and startups is helping organizations integrate agents with CRMs, marketing automation tools and collaboration platforms. Regulatory and industry guidelines around data protection and responsible AI use are also becoming sharper, influencing procurement criteria and vendor selection.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Regulatory environment

The regulatory environment around AI agents is becoming more structured and demanding. Regions such as the European Union are introducing risk‑based frameworks that classify different AI applications and set expectations for transparency, documentation and human oversight. High‑risk uses must meet strict standards for robustness and safety, which directly influences how enterprise‑grade agents are designed and deployed. Organizations need to document how their agents make decisions and how they are tested.

Other major markets, including the United States, the United Kingdom and several Asian countries, are strengthening guidance around data protection, fairness and accountability in AI. This means businesses must consider not only technical performance but also ethical and legal implications. Governance frameworks, audit trails and clear escalation paths are becoming part of any serious agent program. Vendors that build compliance and explainability into their offerings will be better positioned with regulated customers.

Top impacting factors

Several factors are shaping how quickly and widely AI agents spread. The quality and availability of training data strongly affect how well agents understand domain‑specific language and edge cases. Integration with existing systems is another major factor, because agents must talk to CRMs, ERPs, ticketing tools and custom applications to be truly effective. When integration is simple and robust, adoption tends to move faster.

Customer expectations are also a powerful influence. As people become more familiar with conversational AI in consumer apps, they expect similar responsiveness in business settings. If they receive slow or inconsistent service, they may switch providers more quickly. Finally, concerns around security and job impact can slow projects if not addressed with clear communication and safeguards. Successful programs usually combine strong technical execution with careful change management.

Customer Impact: trends and disruptors

From a customer point of view, AI agents are changing what good service looks like. People are getting used to instant, 24/7 access to support and information, often without needing to navigate complex menus. When agents are well designed, customers experience shorter waits, more accurate answers and smoother handovers to human staff when necessary. This raises the bar for all providers in a given market.

At the same time, poor implementations can frustrate customers and damage trust. If an agent cannot understand a question or makes it hard to reach a human, people may feel trapped or ignored. This puts pressure on companies to invest in quality training, testing and escalation design. Over time, customers will likely see AI agents not as a novelty but as the normal first point of contact with brands.

Emerging trends analysis

One important emerging trend is the move from reactive chatbots to proactive, task‑oriented agents. Instead of just answering questions, agents can now detect issues, propose solutions and take actions such as updating records or initiating refunds. In some setups, multiple specialized agents work together, each focusing on a step in a longer process. This shift makes agents more central to how work actually gets done.

Another trend is the rise of industry‑specific agents trained on domain language, regulations and workflows. Healthcare agents, for example, can assist with appointment scheduling and basic triage within strict privacy rules. Financial services agents can help customers navigate complex products and compliance requirements. As these specialized agents improve, they open new opportunities in high‑value, high‑trust environments.

Driver analysis

The strongest underlying driver remains the combination of growing interaction volumes and rising expectations. Customers contact companies through more channels and at more times of day than ever before. Traditional models that rely solely on human agents struggle to scale without large cost increases. AI agents help organizations handle more contacts with stable cost structures.

Labor dynamics also support adoption. Many service organizations face high turnover, long training times and difficulty staffing night and weekend shifts. AI agents provide consistent coverage, reduce onboarding complexity and act as a knowledge backbone for human agents. This combination makes them attractive to leaders who must balance service quality, costs and workforce stability.

Restraint analysis

Despite strong momentum, several restraints still slow adoption. Data privacy and security are top concerns, especially when agents handle sensitive personal or financial information. Organizations must ensure that conversations are stored, processed and shared in line with local laws and internal policies. Breaches or misuse can quickly erode trust and attract regulatory attention.

Another restraint is technical and organizational complexity. Integrating agents with older systems, fragmented data and siloed processes can be challenging. Projects may stall if they require large upfront changes to core systems. In addition, some employees and customers are wary of AI, which can lead to resistance if they feel agents are replacing human roles rather than supporting them.

Opportunity analysis

There are significant opportunities in building agents that are deeply woven into specific industry workflows. In healthcare, agents can support pre‑visit intake, reminders and follow‑up, easing pressure on staff. In insurance, they can streamline claims intake, document collection and status updates. In manufacturing and logistics, agents can help coordinate supply chains, track orders and flag disruptions early.

Another opportunity lies in management platforms that oversee large numbers of agents. As organizations deploy agents across departments, they need tools for monitoring performance, managing versions, enforcing policies and keeping models up to date. Vendors that offer unified visibility, governance and control will become key partners. As regulations mature, solutions that combine strong functionality with clear compliance features will stand out.

Challenge analysis

One ongoing challenge is maintaining trust and quality as agents evolve. Models, data and business rules change over time, and agents must keep up without creating new risks. Organizations need clear processes for testing updates, monitoring live behavior and handling unexpected situations. When an agent reaches the limits of its confidence, it should hand off gracefully to a human.

Another challenge is cultural and organizational adoption. Employees must learn how to work effectively with agents and see them as tools that enhance their roles. Customers must feel that they can always reach a human when needed and that the agent is transparent about its nature and limits. Managing expectations, communicating openly and collecting feedback are crucial to long‑term success.

Top use cases

The most widely adopted use cases today are in customer service and virtual assistants. Agents handle routine questions about orders, billing, account changes and simple troubleshooting across web, mobile and messaging channels. They can guide users through self‑service steps and then pass full context to a human agent if the issue becomes complex. This reduces friction for customers and improves efficiency for support teams.

Outside customer service, AI agents are expanding into IT support, HR and sales. In IT, they reset passwords, check system status and route tickets based on content. In HR, they answer policy questions and help with basic onboarding. In sales and marketing, they qualify leads, recommend products and help customers navigate catalogs. These use cases show how agents can touch almost every part of a business.

Competitive landscape and top key players

The competitive landscape for AI agents includes major cloud providers, enterprise software vendors and specialized AI companies. Large technology firms provide the underlying AI platforms, development tools and integration capabilities that many enterprises rely on. They also offer pre‑built solutions for common use cases such as customer support and IT service management. This combination gives them strong influence over how the market evolves.

Alongside these leaders, established enterprise software vendors are embedding AI agents into CRM, ERP, service and workflow platforms. Companies like Google LLC, IBM Corporation, Microsoft Corporation, Salesforce, SAP SE, UiPath, Amazon Web Services, Oracle Corporation, Zendesk and ServiceNow are central to many deployments. Around them, a wide group of other key players and startups is pushing innovation in multi‑agent systems, low‑code configuration, safety tools and domain‑specific solutions. This mix of global platforms and focused innovators helps the market stay dynamic.

Top Key Players Covered

- Google LLC

- IBM Corporation

- Microsoft Corporation

- Salesforce, Inc.

- SAP SE

- UiPath

- Amazon Web Services, Inc.

- Oracle Corporation

- Zendesk, Inc.

- ServiceNow, Inc.

- Other Key Players

Recent Developments

- In March 2025, EY announced the EY.ai Agentic Platform, created with NVIDIA AI, to deliver domain‑specific enterprise AI agents that blend private reasoning models with human expertise across sectors such as financial services and manufacturing.

- In May 2025, Infosys launched more than 200 enterprise AI agents as part of its Topaz offerings, built on Google Cloud, to transform complex workflows across healthcare, finance, retail, telecom, manufacturing and agriculture

- In August 2025, Wipro reported the completion of a generative AI agent‑building program with Google Cloud, delivering around 200 production‑ready AI agents for industries including banking, insurance and retail.

- In October 2025, Salesforce expanded its Agentforce roadmap under the “Agentic Enterprise” vision, rolling out successive releases that make it easier to embed AI agents into any workflow with enhanced governance, reasoning and voice capabilities.

Conclusion

AI agents have moved into the heart of digital transformation efforts, helping organizations combine smart automation with flexible, conversational interfaces. The strong presence of customer service and virtual assistant use cases, the dominance of enterprise deployments and the leadership of North America all suggest a market that is already scaling fast.

Companies that invest in quality, governance and human‑centered design will gain a meaningful advantage as agents become a familiar part of daily work and customer interactions. Over the coming years, AI agents are set to shape not only how businesses operate but also how people experience brands and services across the world.