Market Overview

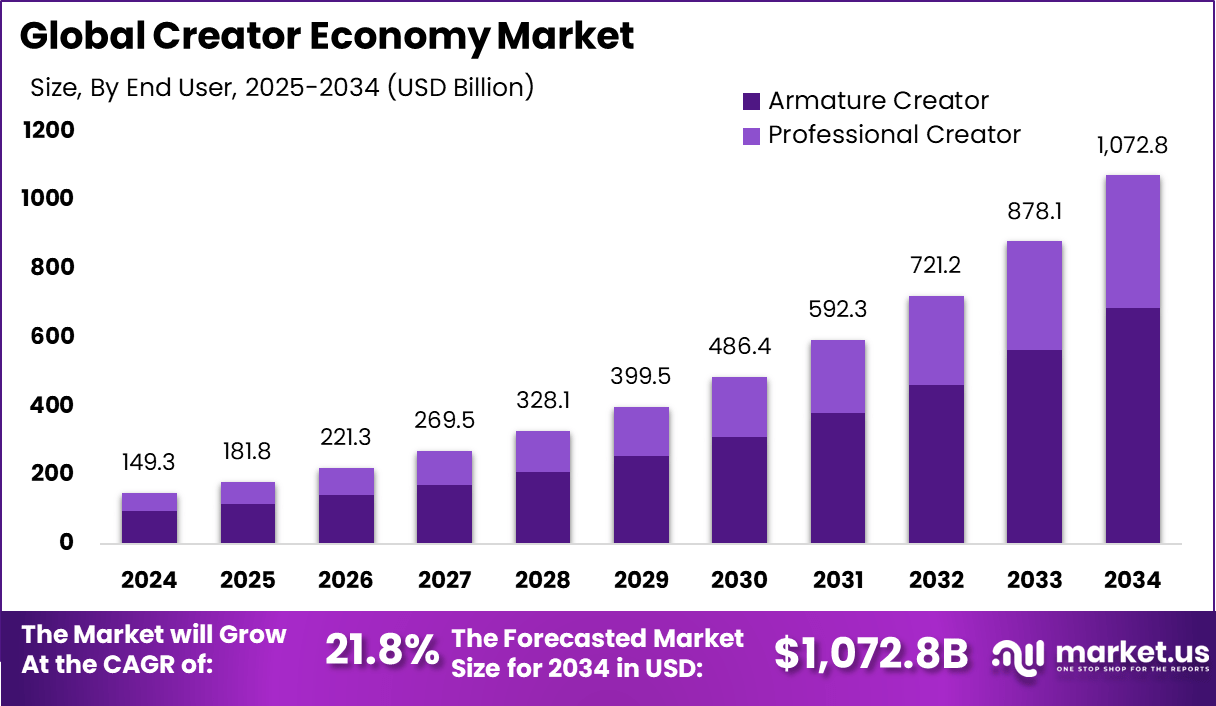

According to Market.us, the Global Creator Economy Market was valued at USD 181.8 billion in 2025 and is projected to reach USD 1,072.8 billion by 2034, growing at a compound annual growth rate (CAGR) of21.8% during the forecast period from 2025 to 2034. This growth reflects a clear shift in how content is produced, shared, and turned into income across digital channels.

The rise of individual creators, from bloggers and podcasters to short-form video producers and live streamers, has turned content creation into one of the fastest-growing segments of the global economy. With over 400 million creators estimated to be active worldwide by 2024, and full-time digital creator jobs in the U.S. growing from 200,000 in 2020 to 1.5 million in 2024, the market shows consistent and sustained forward momentum.

Unlock 2026 Strategic Insights to Support Smarter Decision-Making, Request Here @ https://market.us/report/creator-economy-market/free-sample/

Top Market Takeaways

- Social Media Platforms lead with a 27.8% share, confirming they remain the most preferred base for creators to build, engage, and grow audiences across all content types.

- Video Streaming Platforms hold the second-highest platform share at 24.5%, driven by growing consumer demand for long-form and high-quality video experiences.

- Video content dominates by format type with a 23.8% share, reflecting the strong and steady consumer preference for visual storytelling across platforms.

- Music content follows at 18.3%, boosted by short-form audio formats, independent artists gaining platform access, and steady streaming growth.

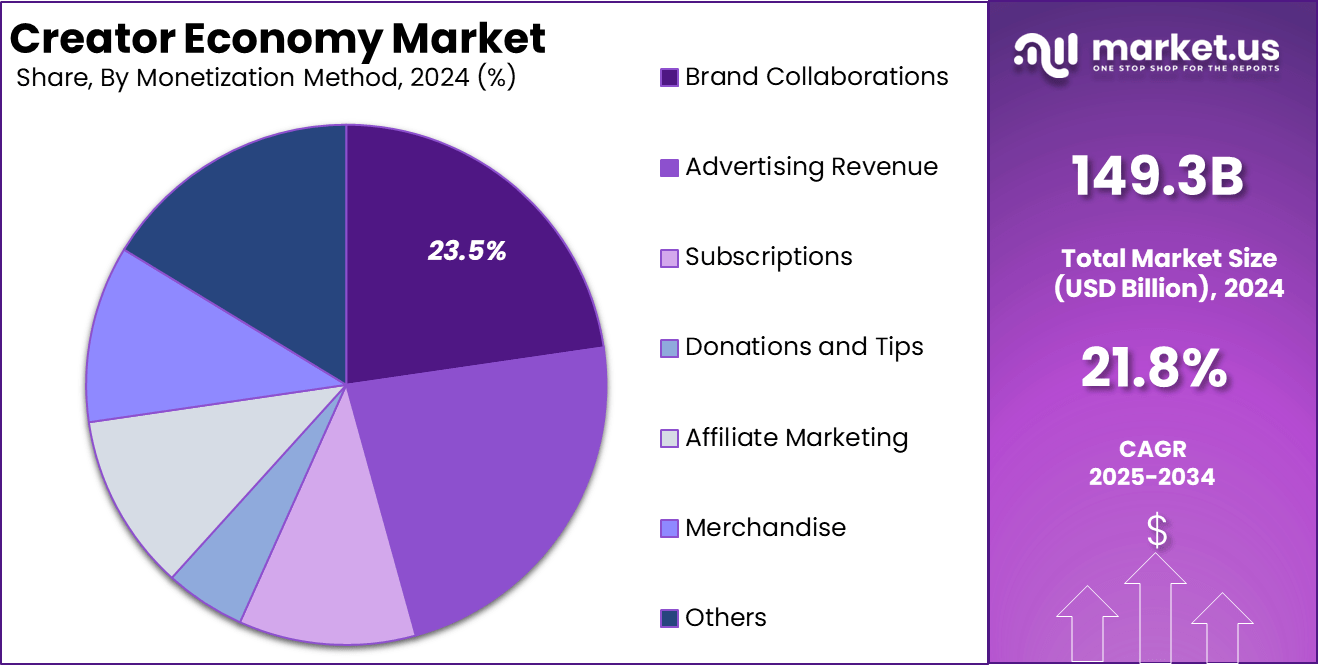

- Brand Collaborations are the top monetization method with a 23.5% share, as brands increasingly partner with creators for genuine audience reach.

- Advertising Revenue stands at 20.9%, remaining a vital income source but slightly behind the more relationship-based brand deal model.

- Amateur Creators form the majority at 64.1%, reflecting low entry barriers and the widespread appeal of content creation as a side income activity.

- Professional Creators account for 35.9%, indicating a well-established and growing segment of full-time content professionals.

- The U.S. Creator Economy is valued at USD 50.9 billion in 2024, with a projected CAGR of 19.3% through 2034, pointing to sustained market growth backed by strong platform investment.

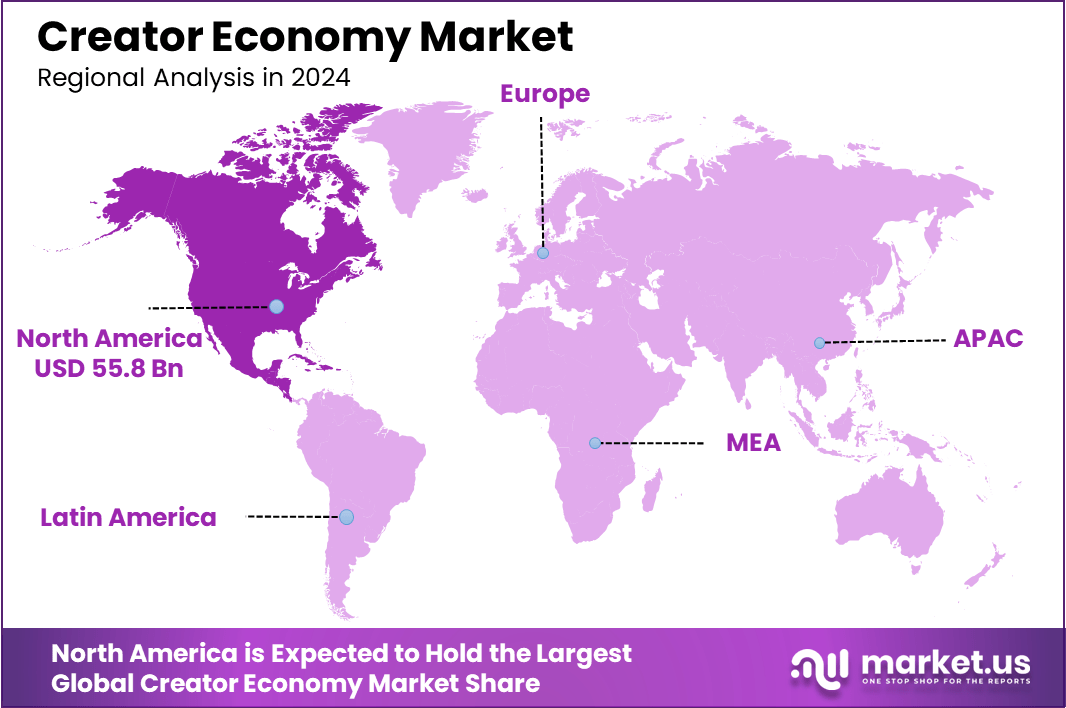

- North America holds a dominant 37.4% share, led by established platforms, built-in monetization tools, and a mature digital infrastructure.

How AI Is Changing the Future of the Creator Economy Market?

Artificial intelligence is no longer a novelty for creators. It has become a core part of how content is made, distributed, and turned into income. As of 2025, 86% of global creators are actively using generative AI tools in their day-to-day work, with the most common uses being content editing and enhancement (55%), generating new images and video assets (52%), and ideation and planning (48%).

More than that, 76% of creators say AI has sped up the growth of their business or follower base, and 81% report being able to produce content they could not have made without AI assistance. This shift is making it easier for smaller and amateur creators to match the production quality that once required professional equipment or large teams.

At the platform level, AI is changing how audiences find and interact with creator content. YouTube reported that over one million channels used its AI creation tools in a single month, and more than 20 million viewers used its Gemini-powered Ask tool to interact with content in new ways.

ByteDance has set aside approximately USD 23 billion in AI investment for 2026, a large portion of which is directed toward improving its creator monetization systems and content recommendation tools. As AI tools become more deeply embedded in creator work, those who adopt them early are likely to build faster, earn more, and hold audience attention at a higher rate than those who do not.

Report Scope

| Report Features | Description |

| Market Value (2024) | USD 149.3 Bn |

| Forecast Revenue (2034) | USD 1,072.8 Bn |

| CAGR (2025-2034) | 21.80% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform (Social Media Platforms, Content-Sharing Platforms, Video Streaming Platforms, Audio Platforms, Gaming Platforms, Others (E-commerce Platforms, etc.)), By Content Type (Video, Written, Gaming, Music, Photography, Art, and Memes, Audio, Others (Educational, etc.), By Monetization Method (Advertising Revenue, Subscriptions, Donations and Tips, Affiliate Marketing, Brand Collaborations, Merchandise, Others), By End User (Professional Creator, Armature Creator) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alphabet Inc., Amazon.com, Inc., ByteDance, Meta Platforms, Spotify AB, Netflix Inc., Snap Inc., Pinterest, Inc., X Corp., Canva, Roblox Corporation, Etsy, Inc., Patreon, Inc., Discord Inc., Substack Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Platform Type Analysis

Social Media Platforms captured more than27.8% of the global creator economy in 2024, leading all other platform categories. This leading position is tied to the size and engagement levels of social media audiences, the range of content formats supported, including short-form video, carousels, and text posts, and the growing sophistication of in-platform monetization tools like tipping, subscriptions, and branded content integrations. North American data supports this finding, with social media holding roughly 29% of platform-based value in the region.

Video Streaming Platforms hold the second-highest platform share at 24.5%. Platforms such as YouTube, Twitch, and emerging competitors have built deep creator monetization environments that go beyond basic ad revenue, offering channel memberships, Super Chats, merchandise integrations, and brand partnership tools. YouTube alone reported over USD 60 billion in combined ad and subscription revenue in 2025, and has paid over USD 100 billion cumulatively to creators, artists, and media partners since 2021.

Share by Platform Analysis (%), 2019-2024

| Platform | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Social Media Platforms | 31.70% | 31.20% | 30.60% | 30.10% | 29.20% | 29.00% |

| Content-Sharing Platforms | 15.30% | 15.20% | 15.20% | 15.10% | 15.10% | 15.00% |

| Video Streaming Platforms | 22.20% | 22.60% | 22.90% | 23.20% | 23.80% | 23.90% |

| Audio Platforms | 12.00% | 12.10% | 12.20% | 12.40% | 12.50% | 12.60% |

| Gaming Platforms | 10.90% | 11.20% | 11.50% | 11.90% | 12.30% | 12.50% |

| Others (E-commerce Platforms, etc.) | 7.90% | 7.70% | 7.50% | 7.30% | 7.10% | 7.00% |

Content Format Type Analysis

Video content leads all format types with a 23.8% share, reflecting its dominance across social media, streaming, and short-form platforms. This is supported by the continued rise of YouTube Shorts, which now averages over 200 billion daily views, and TikTok’s strong grip on short-form viewing patterns globally. Consumers across age groups consistently prefer video as their primary content format, and platforms have responded by building stronger monetization tools specifically for video creators.

Music content follows at 18.3%, driven by independent artists gaining direct platform access, the growth of short-form audio, and active streaming environments. Photography and videography held a 43% share within creative services in 2024, supported by social media culture, influencer marketing demand, and the growing availability of AI-powered editing tools that make professional-quality output accessible to individual creators.

Share by Content Type Analysis (%), 2019-2024

| Content Type | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Video | 21.90% | 22.50% | 23.00% | 23.50% | 24.30% | 24.40% |

| Written | 9.90% | 9.70% | 9.40% | 9.20% | 8.90% | 8.70% |

| Gaming | 17.20% | 17.20% | 17.20% | 17.20% | 17.10% | 17.20% |

| Music | 19.60% | 19.40% | 19.30% | 19.20% | 18.90% | 19.00% |

| Photography, Art, and Memes | 11.20% | 11.00% | 10.90% | 10.70% | 10.60% | 10.40% |

| Audio | 13.30% | 13.40% | 13.60% | 13.70% | 13.90% | 14.00% |

| Others (Educational, etc.) | 6.90% | 6.80% | 6.60% | 6.50% | 6.30% | 6.20% |

Monetization Method Analysis

Brand Collaborations represent the largest monetization method at 23.5%, reflecting a strategic move by marketers toward creator-led content as a more effective and genuine form of brand communication. Brands increasingly recognize that creator audiences are engaged communities, not passive viewers, which makes creator partnerships more efficient than traditional media placements. This category is growing as brands shift to long-term creator relationships rather than one-off promotional posts.

Advertising Revenue at 20.9% remains the second-largest income stream, still a key pillar for creator income across YouTube, podcasting, and display formats. However, ad revenue is subject to platform policy changes and fluctuating CPMs, which has pushed many professional creators to diversify toward more stable income sources like subscriptions, merchandise, and direct fan support.

Share by Monetization Method Analysis (%), 2019-2024

| Monetization Method | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Advertising Revenue | 24.80% | 24.30% | 23.80% | 23.30% | 22.40% | 22.10% |

| Subscriptions | 17.10% | 17.70% | 18.30% | 18.90% | 19.80% | 20.00% |

| Donations and Tips | 7.50% | 7.20% | 7.00% | 6.70% | 6.50% | 6.30% |

| Affiliate Marketing | 12.20% | 12.30% | 12.30% | 12.40% | 12.40% | 12.50% |

| Brand Collaborations | 21.00% | 21.30% | 21.70% | 22.10% | 22.60% | 22.70% |

| Merchandise | 11.60% | 11.60% | 11.50% | 11.50% | 11.30% | 11.40% |

| Others | 5.80% | 5.60% | 5.40% | 5.20% | 5.00% | 4.90% |

Creator Type

Amateur Creators make up the majority at 64.1%, a figure that reflects how accessible content creation has become. With smartphones serving as full production tools for 72% of creators and AI narrowing the production quality gap, the barrier to entering the creator economy has effectively been removed. This segment fuels the top of the funnel, introducing new ideas, formats, and niche communities into the market.

Professional Creators account for 35.9%, representing the structured, full-time part of the market. In the U.S., an estimated 45 million people work professionally as creators, and the number of full-time digital creator jobs has grown sharply from 200,000 in 2020 to 1.5 million in 2024. Despite this growth, income remains uneven. Over 50% of creators earn less than USD 15,000 per year, while a small top group captures a large share of total creator revenue.

End User Analysis

In 2024, the Amateur Creator segment held a dominant market position in the End-User Segment of the Creator Economy Market, capturing more than a 64.1% share. This dominance was largely driven by the explosive rise in individuals creating content for passion, personal branding, or supplemental income rather than as a full-time profession.

The ease of access to smartphones, intuitive video editing apps, and plug-and-play monetization tools on platforms like TikTok, YouTube, and Instagram has made it simple for everyday users to become creators without professional setups or training. The amateur segment’s growth also reflects changing cultural attitudes toward self-expression and digital side incomes.

Share by End User Analysis (%), 2019-2024

| End User | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Professional Creator | 65.40% | 65.00% | 64.50% | 64.10% | 63.50% | 63.30% |

| Armature Creator | 34.60% | 35.00% | 35.50% | 35.90% | 36.50% | 36.70% |

Regional Insights

North America

North America held a dominant 37.4% share of the global creator economy in 2024, making it the largest regional market by a considerable margin.

Share by Region (%), 2019-2024

| Country | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| The US | 92.20% | 92.00% | 91.80% | 91.60% | 91.40% | 91.20% |

| Canada | 7.80% | 8.00% | 8.20% | 8.40% | 8.60% | 8.80% |

This leadership position is supported by mature digital infrastructure, widespread high-speed internet access, an advanced advertising and brand ecosystem, and a long history of platform innovation that has given American creators a structural head start in monetization.

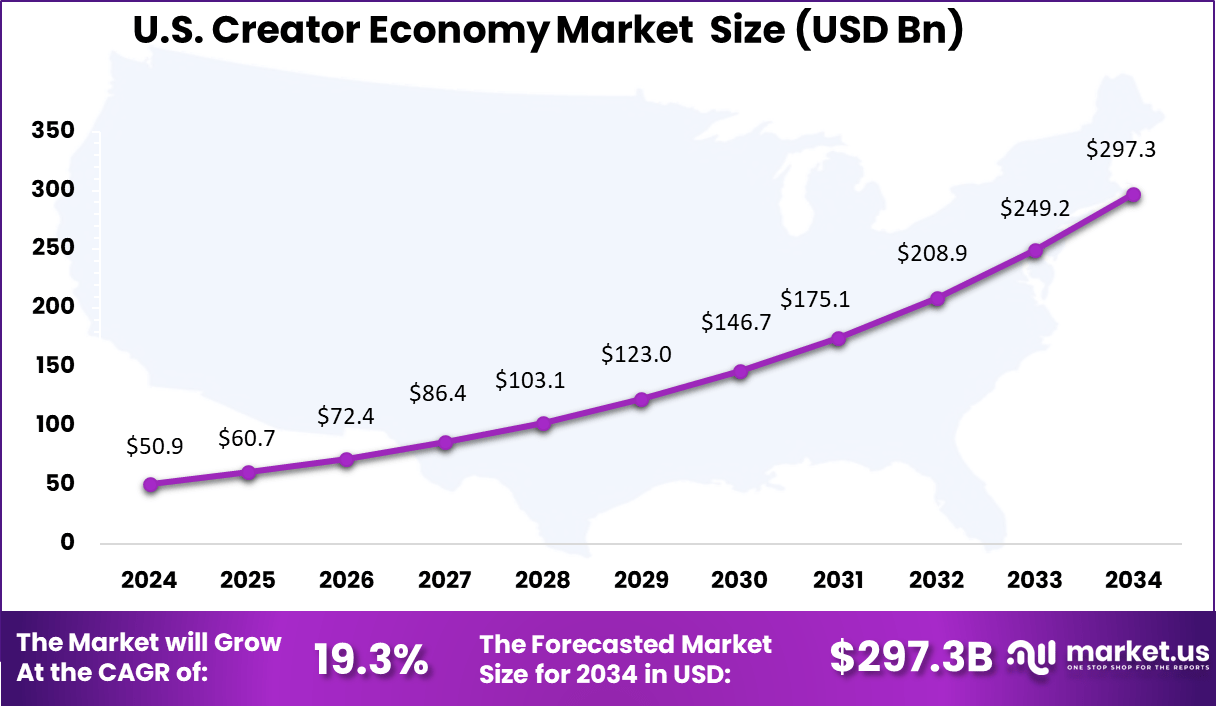

The U.S. Creator Economy was valued at USD 50.9 billion in 2024 and is projected to grow at a CAGR of 19.3%, climbing from an estimated USD 123 billion in 2029 to approximately USD 297.3 billion by 2034.

YouTube’s ecosystem alone contributed USD 55 billion to U.S. GDP in 2024 and supported over 490,000 full-time jobs across the creator and adjacent services sector. Canada complements this market through strong digital adoption rates and a growing base of professional creators across lifestyle, gaming, and educational content categories.

Asia Pacific

Asia Pacific is the fastest-growing region in the global creator economy, forecast to expand at a CAGR of approximately 23.9%, driven by mobile-first content consumption, rapid internet penetration, and growing brand investment in digital creator partnerships. China leads the regional market through platforms like Douyin, Xiaohongshu, and live-streaming commerce integrations that create tightly connected monetization loops between creators and consumers.

India is emerging as a particularly dynamic growth engine, with the India creator economy valued at USD 12.28 billion in 2025 and expected to reach USD 49.83 billion by 2032 at a CAGR of 22.2%. Countries like Indonesia, South Korea, Japan, and Australia are also contributing meaningfully to the regional growth story, supported by expanding smartphone penetration and local language content creation that is drawing in audiences previously outside the creator economy’s reach.

Driver

Democratization of Content Creation Tools

The wide availability of affordable, easy-to-use content creation tools has lowered the barrier to becoming a creator to almost nothing. Smartphones now serve as full production tools for 72% of creators globally, and 75% expect to produce even more content on mobile over the coming year. AI tools have added to this effect by making high-quality output, including editing, scripting, design, and voiceover, possible without expensive software or technical skills.

This has expanded the creator base significantly, with over 207 million content creators worldwide, and the number of full-time digital creator jobs in the U.S. alone growing 7.5 times between 2020 and 2024. As tools become cheaper and more capable, the rate at which new creators enter the market will likely continue to rise, which in turn expands the audience for creator economy platforms and the market for monetization products and services.

Restraint

Platform Dependency and Algorithm Volatility

One of the biggest limits on creator economy growth is the deep dependency creators have on third-party platforms. As of 2026, 51.7% of creators cite algorithm unpredictability as their top professional challenge, ranking it above shrinking brand budgets or competitive pressure. When platforms adjust their recommendation systems, ad policies, or monetization eligibility rules, as YouTube, Instagram, and TikTok do regularly, creators can experience sudden drops in reach and income with little to no warning.

Over 80% of marketers reported having to adjust their influencer strategies because of platform algorithm changes, showing that this instability affects not just individual creators but also the brands that work with them. The concentration of market control in a small number of platforms creates real risk for the whole market. A creator who builds an audience of hundreds of thousands on a single platform is one policy update away from losing access to that audience.

This pattern discourages long-term investment in creator careers and keeps income volatility high. Over 50% of creators earn less than USD 15,000 per year, and while platform diversification is the most common response, managing a consistent presence across multiple platforms takes time and resources that many independent creators cannot sustain.

Opportunity

Social Commerce and Direct-to-Audience Monetization

Social commerce is one of the clearest near-term opportunities in the creator economy. The category is projected to reach USD 2.9 trillion globally by 2026, and creators are positioned as the primary channel through which consumers discover, evaluate, and buy products in a social commerce setting. Unlike traditional e-commerce, social commerce is built into creator content.

Shoppable videos, in-app storefronts, live shopping streams, and affiliate-linked product mentions blend entertainment and retail in a way that traditional advertising cannot match. Platforms are actively building the tools to support this shift. YouTube is working to make shopping a native part of the viewing experience by expanding shoppable ad formats and creator partnership tools.

TikTok’s growing suite of commerce features, including its Shop functionality, is bringing in brands that want to use its highly engaged user base for direct sales. For creators, social commerce adds a transactional income stream that grows with audience size and trust, reducing reliance on ad revenue and brand deal cycles. As brands continue to move larger portions of their marketing budgets toward creator-led commerce, this opportunity will deepen significantly.

Challenge

Content Saturation and Creator Burnout

The same openness that has driven creator economy growth also creates one of its hardest challenges. A market with over 400 million creators by 2024 and platforms that reward frequent posting means creators compete for the same finite pool of audience attention. A 2025 survey found that 52% of creators reported experiencing burnout and 37% considered quitting entirely, citing algorithm pressure, income uncertainty, and the constant demand for more content as the main reasons.

Many creators report that keeping up with the pace that platform algorithms reward comes at the cost of content quality, creative satisfaction, and personal wellbeing. The financial reality adds pressure. Over 96% of creators earn less than USD 100,000 per year, and only 12% of full-time creators make more than USD 50,000 annually. Without better income stability, mental health support, and platform policies that reward quality over frequency, creator burnout is a real threat to the long-term supply of quality content that the whole market depends on.

Competitive Analysis

The competitive market of the global creator economy is built on a small group of platform companies whose infrastructure, audience size, and monetization tools shape the entire industry. Alphabet’s YouTube remains the world’s original and largest creator economy platform, generating over USD 60 billion in combined ad and subscription revenue in 2025, surpassing Netflix to become the world’s largest media company by revenue.

YouTube has paid over USD 100 billion to creators, artists, and media partners since 2021, and its 2026 roadmap focuses on expanding shopping features, broadening the creator partnership hub, and integrating Google’s AI models including Gemini into the creator experience. Meta Platforms, which operates Instagram and Facebook, reported paying creators nearly USD 3 billion in 2025, a 35% year-over-year increase, and has launched new monetization programs designed to attract creators from TikTok and YouTube.

ByteDance, through TikTok and its suite of products including CapCut, reported nearly USD 50 billion in projected net profit for 2025 and plans to invest USD 23 billion in AI in 2026 to improve its creator monetization systems and content recommendation tools. Beyond the platform giants, a strong group of creator-focused companies serves specific segments of the market with dedicated tools, monetization models, and communities.

Spotify has expanded into podcasting and creator monetization, while Netflix, Snap, and Pinterest operate at the meeting point of creator content and brand advertising in their respective content categories. Roblox sits at the intersection of gaming and creator income, building an environment where creators design experiences and earn through in-platform currency.

Top Key Players in the Market

- Alphabet Inc.

- Company Overview

- Product Portfolio

- Financial Performance

- Recent Developments/Updates

- Strategic Overview

- SWOT Analysis

- Note (*): Similar analysis will be provided for other companies as well.

- Amazon.com, Inc.

- ByteDance

- Meta Platforms

- Spotify AB

- Netflix Inc.

- Snap Inc.

- Pinterest, Inc.

- X Corp.

- Canva

- Roblox Corporation

- Etsy, Inc.

- Patreon, Inc.

- Discord Inc.

- Substack Inc.

Recent News and Developments

- Alphabet (YouTube): In early 2026, YouTube CEO Neal Mohan laid out a creator-focused vision built around three areas: expanded shopping within Shorts, AI-powered creation tools for all channel types, and a redesigned creator partnership hub to simplify brand collaboration at scale. YouTube Shorts now averages over 200 billion daily views and is earning more revenue per watch hour than traditional in-stream ads in several major markets including the U.S.

- Meta Platforms: In March 2026, Meta confirmed it paid creators USD 3 billion through its monetization programs in 2025, a 35% jump from 2024 and its highest annual creator payout on record. The company also launched a new monetization initiative specifically targeting creators from TikTok and YouTube, offering direct financial incentives and improved content visibility on Facebook as part of its effort to strengthen its position in the creator market.

- ByteDance (TikTok): ByteDance reached an agreement in early 2026 to restructure TikTok’s U.S. business into a new entity, TikTok USDS Joint Venture LLC, with Oracle, Silver Lake, and Abu Dhabi’s MGX collectively holding approximately 45% of the new company. Despite ongoing regulatory uncertainty, ByteDance’s global revenue is targeting approximately USD 186 billion in 2025, roughly 20% higher year-over-year.