Introduction

Valvoline Statistics: Valvoline Inc has become the leading company in preventive automotive maintenance through its quick-lube service model and its extensive retail network. The company achieved consistent financial progress and operational success while expanding its operations throughout North America during the 2025-2026 period.

Valvoline strengthens its market position because of increasing vehicle ownership and growing maintenance service demand, and its efforts to increase same-store sales. The company’s performance shows its ability to withstand challenges because of continuous revenue growth, rising EBITDA margins and network development.

The article examines essential statistics, financial information and research findings that determine Valvoline’s growth path.

Editor’s Choice

- Valvoline revenue grew from USD 1,037M (2021) to USD 1,710M (2025), marking ~65% cumulative growth.

- The company achieved an approximate 13% annual revenue growth rate over five years.

- Adjusted EBITDA increased from USD 277.0M (2021) to USD 466.8M (2025), a ~68% rise.

- The continuing operations income reached about USD 214.8 million in 2025 after experiencing unstable periods.

- The organization has 11400 employees, with approximately 89% working in retail.

- The average store staffing efficiency across 1016 stores reaches approximately 10 workers per location.

- Same-store sales reached their highest point of 21.2% during 2021, which represented a roughly ninefold increase compared to 2020 (2.3%).

- SSS normalized to 6.1% by 2025, remaining above pre-2018 levels.

- The company expanded its store network from 1068 locations in 2016 to 2180 locations in 2025, which represents a total growth rate of approximately 104%.

- Company-owned stores increased by approximately 197% while franchise operations grew by only 60%.

- The company returned about 96% of shareholder value between 2020 and 2025, which exceeded the performance of benchmark indexes.

- The company achieved a gross profit of USD 658.5 million during 2025, which represented a 6.4% increase compared to the previous year.

- The company experienced a USD 24.2 million increase in operating cash flow because its interest expenses decreased by USD 22.1 million.

- Share count declined ~21% (2023–2025), boosting EPS accretion.

- The Breeze Autocare acquisition adds 162 net stores for USD 593M, which the company will finance through its USD 740M Term Loan B.

Valvoline Revenue

(Reference: q4cdn.com)

- Valvoline shows strong and continuous revenue growth, which demonstrates both its stable business structure and its growing market share.

- Net revenues increased from USD 1,037 million in 2021 to USD 1,710 million in 2025, representing an impressive 65% cumulative growth over five years.

- The company experienced revenue growth throughout the year, which reached USD 1,236 million in 2022, USD 1,444 million in 2023 and USD 1,619 million in 2024 before reaching its highest point in 2025.

- The automotive lubricants market and service segments show strong demand, which results in an approximate annual growth rate of 13% for the company.

- Valvoline demonstrates strong operational capabilities through its financial results, which show consistent revenue growth to establish the company as a rapidly expanding business in the worldwide lubricants and automotive services market.

Valvoline Profitability Acceleration & EBITDA Expansion

(Source: q4cdn.com)

- The financial trajectory of Valvoline shows an impressive growth story because the company achieves operational efficiency while expanding premium services, and the automotive aftermarket shows strong demand.

- The company’s income from continuing operations shows unpredictable patterns which later develop into stable growth.

- After declining from USD 200.1 million in 2021 to USD 109.4 million in 2022 (a ~45% drop), Valvoline rebounded sharply to USD 199.4 million in 2023, signaling recovery momentum.

- The company maintained its upward trend through 2024, when it reached USD 214.5 million and through 2025, when it achieved USD 214.8 million, which showed stable profits and better expense management.

- The main profitability measure, Adjusted EBITDA, demonstrates continuous development of sustainable growth.

- The company’s EBITDA increased from USD 277.0 million in 2021 to USD 466.8 million in 2025, which resulted in about 68% growth during the five-year period.

- The consistent growth from USD 315.7M in 2022 to USD 380.0M in 2023 and USD 442.6M in 2024 demonstrates the company’s ability to achieve better profit margins through improved operational efficiency and responsible financial management.

- Valvoline maintains its financial stability through its commitment to quick-lube services, its retail business growth and its dedication to developing solutions that meet customer needs.

- The company will benefit from increasing vehicle maintenance requirements because it maintains consistent revenue streams and experiences fast EBITDA growth in high-demand areas.

- Valvoline shows strong financial prospects because its business operations maintain fundamental strength and the ability to expand and generate continuous revenue growth.

Valvoline Workforce

(Source: q4cdn.com)

- Valvoline’s 2025 workforce structure operates through retail operations, which utilize centralized functions that operate with minimal yet sufficient resources.

- The company maintains stable employment across its North American operations with 11400 employees who include 10600 full-time workers.

- Valvoline uses its service centers to provide customer service and retail operations, which results in 10100 employees who work at company-owned locations.

- The company operates 1016 stores, resulting in an average of 10 employees per store to achieve efficient service delivery through effective labor management.

- The company has 1300 employees who work in corporate supply chain management, digital operations, marketing and strategic planning as the central support team. This segment, which operates at a smaller size, plays a vital role in expanding operations across a network of approximately 2200 stores, which includes franchised locations.

Valvoline Same-Store Sales Surge

(Source: q4cdn.com)

- The Valvoline system displays a same-store sales (SSS) growth pattern which develops through four stages, including its initial period of continuous growth, its period of pandemic-related interruptions, its time of rapid recovery, and its process of moving toward normal operations.

- The pre-pandemic period between 2016 and 2019 shows analysts that the organization experienced stable growth, which reached 10.1% in 2019 after starting from 7.5% in 2016, because of network expansion, customer retention and increasing vehicle maintenance needs.

- The year 2020 experienced a major decline because SSS growth dropped to 2.3% through the impacts of COVID-19 and the decrease in public movement.

- The 2021 recovery achieved exceptional results through a 21.2% peak growth, which represented a 9x increase over 2020 because of pent-up demand, economic reopening and increased service consumption.

- The growth pattern after 2021 shows a trend toward normalcy, which starts with 14.0% growth in 2022 and 12.2% growth in 2023 and 7.1% growth in 2024 and 6.1% growth in 2025.

- The post-2018 period shows a demand and pricing power that stays strong because these numbers continue to exceed their previous pre-2018 levels.

- Valvoline’s SSS results demonstrate a strong business model which enables the company to survive economic challenges while it continues to grow its revenue and maintain its retail operations.

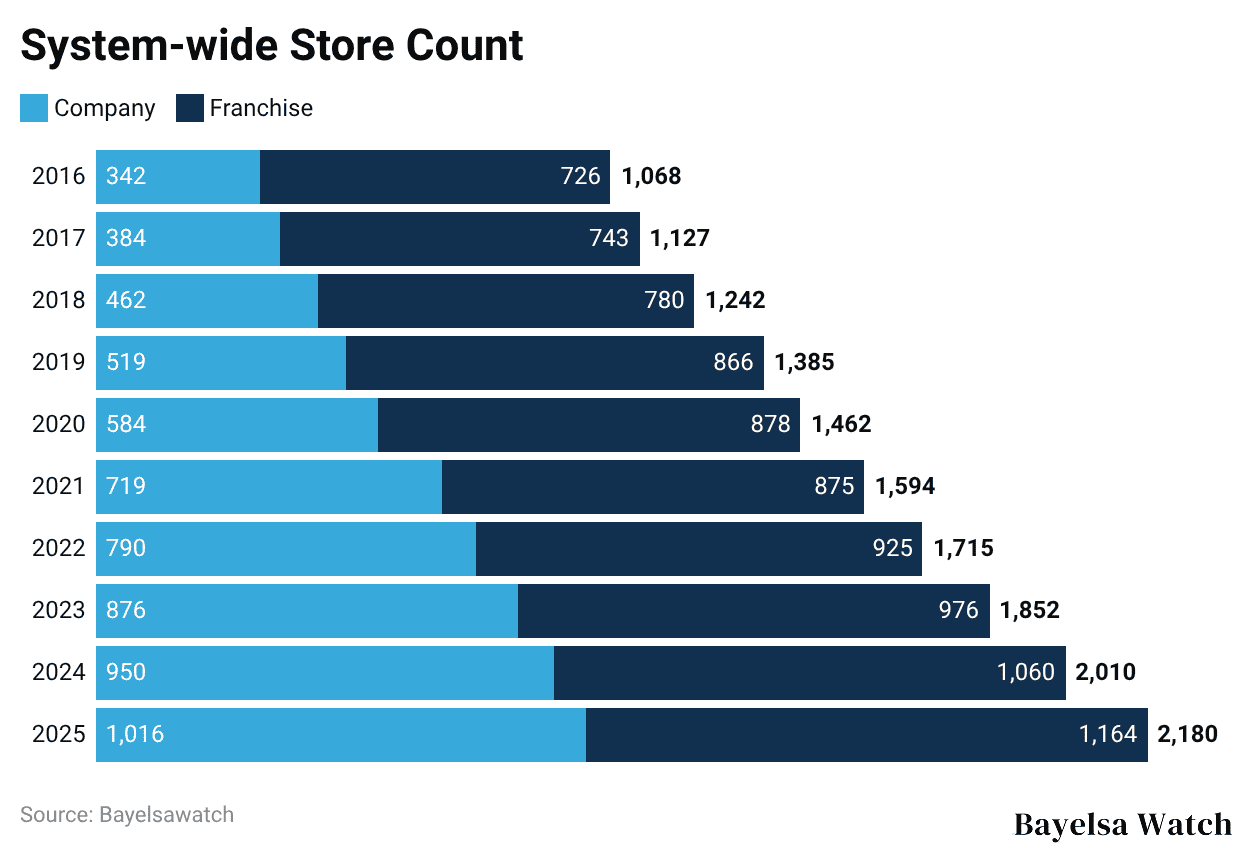

Valvoline Store Footprint Growth & Franchise-Led Scalability

(Reference: q4cdn.com)

- Valvoline demonstrates successful business expansion through its system-wide store growth, which results from both its company-operated stores and its franchise partnerships.

- The total store count has nearly doubled from 1,068 in 2016 to 2,180 in 2025, representing an impressive ~104% growth over nine years, highlighting strong retail penetration and market scalability.

- The current situation shows that the business operates a combination of company-run facilities and franchise business locations, which continues to develop according to changing market conditions.

- Company-owned locations grew from 342 in 2016 to 1,016 in 2025, marking a ~197% increase, significantly outpacing franchise growth.

- Franchise stores grew from 726 to 1,164, which represents a steady ~60% increase, which supports Valvoline’s expansion model that requires fewer physical assets.

- The period from 2020 until 2023 shows rapid business expansion, which resulted in total stores growing from 1,462 to 1,852, because of strategic business acquisitions, new store openings and strong franchise partnerships.

- The company-operated stores will make up approximately 47% of the entire network by 2025, which represents an increase from 32% in 2016, thus indicating a company trend toward better operational management and profit margin control.

- Valvoline expands its business operations through its various distribution channels while running a successful retail operations system that uses both company ownership and franchise partnerships to create new revenue streams and enhance brand recognition and sustainable business profits.

Valvoline Market Outperformance

(Source: q4cdn.com)

- The cumulative shareholder return performance of Valvoline shows three components, which include market outperformance, cyclical volatility, and long-term value creation.

- Valvoline returned USD 195.79 from a 2020 base investment of USD 100, which generated approximately 96% total returns that exceeded both the S&P MidCap 400 Index return of USD 189.26 and the S&P MidCap 400 Speciality Retail Index return of USD 179.91.

- Valvoline achieved strong momentum during its early stage, which led to its stock price reaching USD 166.78 in 2021 while surpassing market index performance.

- The market entered a correction phase during 2022, which caused returns to drop to USD 137.63 because of economic downturns, rising inflation and market unrest.

- The company experienced a strong recovery during 2023, which brought its value to USD 175.78 before reaching its highest point of USD 228.17 in 2024, which represents a 128% increase from the original value.

- The 2025 returns decreased to USD 195.79 because traders took profits and markets reached their typical state, yet the company still maintained its superior status against market benchmarks.

- The trajectory of this research study uses primary keywords, which include shareholder return, stock performance, market comparison, and investment growth and volatility trends.

- Valvoline shows a strong stock performance, which demonstrates an enduring equity performance that delivers substantial long-term financial returns to shareholders through its successful recovery periods and market comparison.

Valvoline Gross Profit

(Source: q4cdn.com)

- The gross profit evolution of Valvoline between 2024 and 2025 shows that revenue growth drivers and cost headwinds maintain equal forces.

- Gross profit increased from USD 618.8 million in 2024 to USD 658.5 million in 2025, which resulted in a USD 39.7 million uplift that showed financial stability and business growth capacity.

- Volume expansion served as the main growth driver, which produced a revenue increase of USD 43.3 million because the company expanded its store network, while more customers visited its locations.

- The service mix, together with non-oil change services, saw premiumization growth, which produced a revenue increase of USD 23.8 million.

- A smaller contribution from acquisitions, which produced a revenue increase of USD 2.7 million, supported growth.

- The price and cost impacts showed -USD 11.1 million, which demonstrates the effects of rising input costs and inflationary pressure, while dispositions show -USD 18.7 million, which shows the financial effects from ongoing refranchising activities.

- Currency exchange had a minimal negative effect of -USD 0.3 million.

Valvoline Cash Flow Dynamics

(Source: q4cdn.com)

- Valvoline generates cash from its core business operations through a balanced approach which aims to increase its earnings while funding its growth and managing its debt.

- The company shows better cash flow production through its financial operations, which use responsible spending practices according to the analyst assessment.

- The company achieved a USD 24.2 million increase in operating cash flows during the previous year because of its improved cash earnings and better operational results.

- The company experienced a major effect, which resulted from decreasing interest expenses by USD 22.1 million because its debt obligations went down after it finished its previous debt reduction initiatives.

- The company experienced growth, which became smaller because its working capital needs increased through higher acquisition costs and divestiture expenses, which created temporary cash flow problems that stemmed from its current strategic changes.

- The company experienced a major cash flow decrease during its investing activities, which totalled USD 337.9 million, because its investment proceeds dropped by USD 345.0 million after the previous year, when it sold Global Products.

- Valvoline dedicated USD 12.3 million to acquisition costs and USD 34.8 million to capital investments, which demonstrate its commitment to expanding its store network, improving its infrastructure and making long-term growth investments.

- The company used asset sales, which included refranchising transactions, to reduce cash outflows by USD 49.5 million.

- Cash outflows from financing operations decreased by USD 633.4 million because the company reduced its debt payments by USD 480.0 million and cut its share repurchase costs by USD 166.4 million. This change shows that the company now prioritizes protecting its capital and maintaining a strong financial position.

Valvoline Earnings Per Share

(Source: q4cdn.com)

- The Valvoline EPS profile shows two different financial aspects of the company. The basic EPS performance shows continuous growth from 2023 to 2025, with an increase from USD 1.24 to USD 1.65 in 2024 and USD 1.68 in 2025, which shows approximately 35% growth during this period.

- The diluted EPS from continuing operations increased from USD 1.23 in 2023 to USD 1.67 in 2025, which shows the company experienced stable earnings growth while maintaining consistent profit margins and effective business operations.

- The upward trend matches the income stability from continuing operations, which reached USD 214.8 million in 2025.

- The total EPS results show strong dependency on discontinued operations because the 2023 results include a USD 1.22 billion gain, which raised basic EPS to USD 8.79 and produced a high base effect.

- The 2024 and 2025 periods showed minor losses from discontinued operations, which resulted in total EPS adjustments to USD 1.63 and USD 1.65, respectively.

- The company reduced its weighted average shares outstanding from 161.6 million in 2023 to 127.9 million in 2025 through share repurchases, which created value for shareholders and boosted EPS growth.

Recent Developments

- The latest strategic changes at Valvoline demonstrate their dual operational strategy, which they use to optimize existing assets and pursue growth through external acquisitions.

- The refranchising strategy creates capital efficiency improvements, which lead to better returns on invested capital (ROIC) and faster market expansion through local franchise proficiency.

- The acquisition of Breeze Autocare by Valvoline serves as a major engine for business development. Valvoline will acquire 200 service centers through this deal, which costs USD 625 million, thus expanding its presence in key U.S. markets, including California and Texas.

- The company must divest 45 stores to meet Federal Trade Commission requirements, which create regulatory oversight but allow for a net business growth.

- The company transaction depends on a USD 740 million Term Loan B, which demonstrates how the organization uses strategic leverage to fund its operations while using extra funds for debt settlement and maintaining its financial stability.

- The current phase of the project uses primary keywords, which include refranchising strategy, acquisition growth, capital allocation, retail expansion, and operational scalability to define its elements.

- Valvoline achieved successful portfolio management through its combination of business restructuring efforts and expansion activities, which enabled the company to achieve sustainable revenue growth and improve profit margins while creating long-term value for shareholders.

Capital Allocation & Financial Metrics Overview

| Capital Allocation Metric | Fiscal 2023 | Fiscal 2024 | Fiscal 2025 | ~2,5x (est.) |

| Share repurchases | USD 1.6B+ (incl. tender offer). | USD 15M. | ~USD 60M (paused Q2 FY2025). | USD 0 (buyback suspended). |

| Remaining buyback authorization | N/A | ~USD 385M | USD 325M at Q2 FY2025 (frozen). | USD 325M (still authorized but inactive). |

| Total reported debt | — | ~USD 620M (est.) | USD 1,074M (pre-Breeze close). | ~USD 1.7B (post-Term Loan B). |

| Rating-agency adjusted leverage | — | ~2.5x (est.) | 3.4x (FY2025 year-end). | ~4.2x (pro-forma post-Breeze) |

| S&P-adjusted leverage (projected peak) | — | — | — | 4.7x (FY2025 reported); 4.4x pro-forma. |

| Target leverage range | 2.5x–3.5x | 2.5x–3.5x | 2.5x–3.5x | 2.5x–3.5x (expected by late 2026). |

| Breeze acquisition price (net) | — | — | USD 593M net (162 stores). | Closed December 1, 2025. |

| Term Loan B issued | — | — | USD 740M (at closing). | Outstanding; floating rate; covenant-lite. |

| Acquisition multiple | — | — | 10.7x Breeze adjusted EBITDA. | Synergies are expected to improve effectiveness over time. |

Valvoline Future Outlook

- The long-term investment narrative of Valvoline faces a challenge from electric vehicle (EV) disruption worries, which fail to show the actual strength of the company because its business model keeps adapting to market needs.

- The global automotive market continues to depend on internal combustion engine (ICE) vehicles, which create permanent demand for Valvoline core services until 2030.

- Earnings per share (EPS) show financial stability because it reflects strong profitability, which originates from ongoing operations that will produce approximately USD 214 million in 2025, and the company has decreased its share count by 21% since 2023, which leads to greater EPS growth and increased value for shareholders.

- Valvoline operates two thousand four hundred service centers, which provide over thirty million annual services that produce revenue of USD 1.7 billion with a yearly growth of 12%. The main search terms which define the study show growth in revenue, stable EPS, base service increases and better operational performance.

- Valvoline establishes its position in the fast-growing EV fluids market through its offering of 12-volt battery replacement services and EV-specific fluids and hybrid vehicle oils.

- The services exist because vehicle technologies evolve, and the company uses its quick-service retail model.

- Management predicts fiscal year 2026 performance through a 4 to 6 % same-store sales increase, approximately 20 % revenue increase and approximately 15 % EBITDA growth, which demonstrates their faith in business expansion through existing operations.

- Valvoline maintains market presence because it implements strategic changes which protect its earnings power while creating permanent growth.

Conclusion

The company Valvoline shows strong business growth through two critical factors, which include its increasing revenue, growing EBITDA, and expanding retail network. The company maintains operational advantages through its existing vehicle base, which relies on internal combustion engines and its need to provide essential vehicle maintenance services. The company enhances its market reach through its refranchising and acquisition strategies, which improve capital efficiency.

Valvoline establishes its long-term market position through its expansion into electric vehicle service and fluid product offerings. The company demonstrates strong potential for sustainable profitability and shareholder value creation through its stable earnings, effective cash flow management, and ongoing same-store sales growth in the changing automotive industry.

FAQ

Valvoline’s revenue increased from USD 1.04B to USD 1.71B, reflecting ~65% growth over five years.

The company reported USD 466.8M EBITDA and USD 214.8M income from continuing operations, showing strong profitability.

Valvoline operates approximately 2180 stores worldwide through its company-owned stores and franchise partnerships.

Valvoline expands its business into electric vehicle fluids and battery services, while most vehicles today still use internal combustion engines despite rising electric vehicle adoption.

Valvoline acquired Breeze Autocare for USD 593M, adding 162 net stores to accelerate growth.